![]()

Search Market Research Report

Artificial Intelligence (AI) Sensors Market Size, Share Global Analysis Report, 2024 – 2032

Artificial Intelligence (AI) Sensors Market Size, Share, Growth Analysis Report By Type (Pressure, Temperature, Optical, Position, Ultrasonic, Motion, Navigation, and Others), By Technology (NLP, Machine Learning, Computer Vision), By Application (Automotive, Consumer Electronics, Manufacturing, Aerospace and Defense, Robotics, Smart Home Automation, and Others), And By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2024 – 2032

Industry Insights

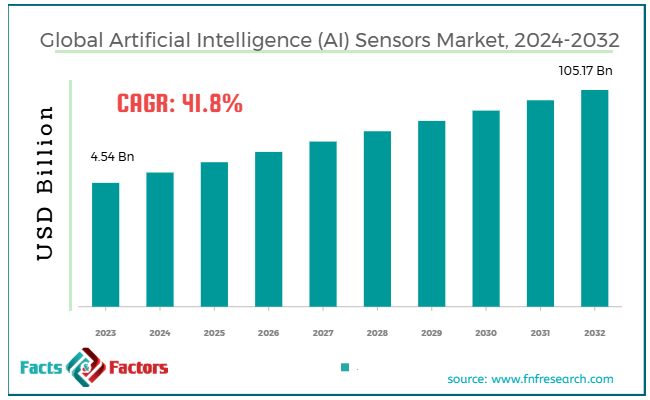

[221+ Pages Report] According to Facts & Factors, the global artificial intelligence (AI) sensors market size was worth around USD 4.54 billion in 2023 and is predicted to grow to around USD 105.17 billion by 2032, with a compound annual growth rate (CAGR) of roughly 41.8% between 2024 and 2032.

Market Overview

Market Overview

Artificial intelligence (AI) sensors are devices embedded with AI algorithms to understand and interpret information from the physical world. These sensors gather data from their surroundings and apply AI skills for analysis, mostly for making predictions or decisions in real-time. The key driver of the global artificial intelligence (AI) sensors market is the increasing demand for smart and automation systems in different sectors.

Moreover, other leading drivers comprise the growing adoption of IoT, the growth of autonomous vehicles, and improvements in technologies. The IoT network is majorly dependent on AI sensors to collect, study, and respond to data. The rising proliferation of smart systems and connected devices is fueling the demand for AI sensors.

Also, autonomous vehicles rely on AI sensors like cameras, LiDAR, radar, and ultrasonic sensors to understand their surroundings and make decisions. The rising investments in self-driving vehicles are notably impelling AI sensor demand. Improvements in sensor and AI technologies, like edge computing, ML, and sensor miniaturization, are driving the modernization of AI sensors.

Nonetheless, a few factors restraining the growth of the global market include security & privacy concerns and inadequate standardization. AI sensors collect massive quantities of sensitive and personal data, which increases security concerns. Hence, ensuring protection from cyber threats is a key challenge. Any breach might compromise the trust and safety of AI systems, mainly in crucial sectors like healthcare.

Moreover, the lack of uniform protocols and standards for different kinds of AI sensors makes it challenging for businesses to integrate them into their systems. This significantly hampers the scalability and interoperability of AI sensors.

Yet, the market will witness major growth over the estimated period owing to the growing applications in smart cities and rising integration with edge computing. AI sensors are vital parts of smart cities, with applications in waste management, traffic management, energy efficiency, and environmental monitoring.

With the growing development of smart cities, the adoption of AI sensors is also surging, thus impacting market growth. Also, incorporation with edge computing offers opportunities for faster processing and decision-making in real-time.

Key Insights:

- As per the analysis shared by our research analyst, the global artificial intelligence (AI) sensors market is estimated to grow annually at a CAGR of around 41.8% over the forecast period (2024-2032)

- In terms of revenue, the global artificial intelligence (AI) sensors market size was valued at around USD 4.54 billion in 2023 and is projected to reach USD 105.17 billion by 2032.

- The artificial intelligence (AI) sensors market is projected to grow significantly owing to the increasing demand for industrial automation, improvements in sensor and AI technologies, and burgeoning use in healthcare for diagnostics, treatment optimization, and patient monitoring.

- Based on type, the optical segment is expected to lead the market, while the motion segment is expected to register considerable growth.

- Based on technology, the machine learning segment is the dominating segment among others, while the computer vision segment is projected to witness sizeable revenue over the forecast period.

- Based on application, the automotive segment is expected to lead the market compared to the consumer electronics segment.

- Based on region, North America is projected to dominate the global market during the estimated period, followed by Europe.

Growth Drivers

- Improvements in self-driving vehicles fuel the artificial intelligence (AI) sensors market growth

Self-driving vehicles are largely dependent on AI sensors like cameras, LiDAR, and ultrasonic sensors to understand ambiance and make decisions in real-time. As the automotive sector is shifting towards complete autonomy, the need for AI sensors to allow safety, navigation, and interaction is burgeoning.

AI sensors in autonomous cars allow vital functions like collision avoidance, lane-keeping distance, and object detection.

The global autonomous vehicle industry is projected to gain momentum and reach $ 1556.67 billion by 2030 with a 56.3% CAGR.

Hesai Technology, a prominent manufacturer of LiDAR, lately declared its plans to decrease the cost of LiDAR sensors. They aim to make it more accessible for bulk production in self-driving cars. This price reduction is anticipated to fuel the adoption of AI sensors, affecting artificial intelligence (AI) sensors market growth.

- Growing demand for industrial automation to contribute to the market growth

The inclination towards automation is fueling the use of AI sensors. Producers are increasingly using AI sensors for predictive maintenance, process automation, improved efficiency, and quality control. These sensors offer actionable insights and allow monitoring in real-time, aiding the optimization of production lines and decreasing human interference. AI sensors are increasingly adopted in predictive maintenance to help manufacturers decrease equipment failure and enhance operational efficacy.

The adoption of AI-based robots in sectors like logistics and manufacturing is growing substantially. Brands like BMW and Tesla are using AI sensors to reduce human labor costs, automate factory operations, and enhance precision.

Restraints

- Technical limitations in power consumption and sensor accuracy unfavorably impact the progress of the artificial intelligence (AI) sensors market

Despite major improvements in AI sensors, they still lack precision, energy efficiency, and resolution, hampering the artificial intelligence (AI) sensors market growth.

For example, several AI sensors face challenges to perform precisely in high-noise and low-light environments. They also consume high energy, mainly in battery-operated or remote devices. The growth of low-power algorithms and edge computing is resolving such issues. Leading companies like Qualcomm and NVIDIA are making efforts to produce fuel-efficient AI solutions or sensors.

Furthermore, prominent companies like Apple and Google have started using AI to enhance the performance of sensors and decrease energy consumption in smart devices. But, these efforts are currently under development and are yet to be standardized in the industry.

Opportunities

- AI sensors in predictive maintenance and industrial automation positively affect the artificial intelligence (AI) sensors market growth

Industrial automation is among the leading opportunities for artificial intelligence sensors, mainly in process optimization, predictive maintenance, and quality control. In manufacturing plants, AI sensors can effectively detect possible equipment failure beforehand, allowing companies to avoid expensive downtime and take preventive measures.

General Electric (GE) and Siemens are increasingly investing in artificial intelligence technologies to improve predictive maintenance and automation capabilities in the transportation, manufacturing, and energy sectors.

Bosch introduced AI-based predictive maintenance systems for factories in 2023. It used modernized sensors to constantly predict failures and monitor equipment performance, thus reducing costs and improving efficiency.

Challenges

- Interoperability and integration issues restrict the growth of the artificial intelligence (AI) sensors market

AI sensors are frequently integrated into current systems like smart devices, IoT platforms, and self-driving vehicles. Interoperability in different AI-based sensor technologies and lack of standardization are among the key challenges. This may complicate companies to produce systems that perform smoothly on different platforms. The lack of common standards in AI and sensor technology challenges the incorporation of sensors in diverse software and hardware systems. This results in higher costs and prolonged deployment time.

Report Scope

Report Attribute |

Details |

Market Size in 2023 |

USD 4.54 Billion |

Projected Market Size in 2032 |

USD 105.17 Billion |

CAGR Growth Rate |

41.8% CAGR |

Base Year |

2023 |

Forecast Years |

2024-2032 |

Key Market Players |

Nvidia Corporation, Intel Corporation, Texas Instruments, Honeywell International Inc., Bosch Sensortec GmbH, STMicroelectronics, Qualcomm Technologies Inc., Analog Devices Inc., Infineon Technologies AG, Renesas Electronics Corporation, Omron Corporation, Xilinx Inc., Toshiba Corporation, Flir Systems Inc., Sony Corporation, and Others. |

Key Segment |

By Type, By Technology, By Application, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Segmentation Analysis

- The global artificial intelligence (AI) sensors market is segmented based on type, technology, application, and region.

Based on type, the global artificial intelligence (AI) sensors industry is divided into pressure, temperature, optical, position, ultrasonic, motion, navigation, and others. In 2023, the optical sensors segment registered a notable share of the artificial intelligence (AI) sensors market and is expected to continue dominance over the forecast period as well. This leading growth is attributed to their vital role in uses like smartphones, autonomous vehicles, healthcare diagnostics, and wearable devices. These sensors are used to detect and interpret light to allow tasks (environment mapping, facial recognition, and object recognition) and vision systems.

Optical sensors play a crucial role in healthcare, in non-invasive diagnostics like pulse oximeters and blood glucose monitoring. In consumer electronics, sensors allow gesture recognition and AR experiences.

Based on technology, the global artificial intelligence (AI) sensors industry is segmented as NLP, machine learning, and computer vision. The machine learning segment held a major market share in the previous year, owing to its growing significance in the majority of AI applications. These sensors are dependent on ML algorithms to efficiently process massive data and enhance decision-making with no special programming. ML allows these sensors to learn from the surroundings, improve system performance, and make predictions.

ML algorithms are important in predictive maintenance, predictive analysis, and data-based decision-making in diverse sectors.

Based on application, the global market is segmented as automotive, consumer electronics, manufacturing, aerospace and defense, robotics, smart home automation, and others. The automotive segment is projected to lead the market owing to its vital role in revolutionizing the industry. This comprises applications like ADAS, autonomous driving, and vehicle automation.

Sensors like cameras, LiDAR, ultrasonic sensors, and radars are important for enhancing car safety features like lane-keeping assist, collision avoidance, and adaptive cruise control. The need for driverless cars and advanced driver assistance systems has been propelled by technology companies, and vehicle manufacturers are aiming to develop cars with self-driving abilities. These technologies are highly dependent on AI sensors, thus impelling the growth of the artificial intelligence (AI) sensors market.

Regional Analysis

- North America to witness significant growth over the forecast period

North America has held a remarkable share of the global artificial intelligence (AI) sensors industry in previous years and is projected to lead in the future as well. The key reasons for the growth include strong industrial adoption, technological advancements and innovations, and heavy investments. The region, especially the United States, is leading due to the presence of prominent companies like Apple, Nvidia, Google, and Tesla, which use AI sensors on a larger scale. The region established major strides in self-driving vehicles, healthcare applications, industrial automation, and smart homes, all of which use AI sensors.

Furthermore, Canada and the U.S. are forerunners in the adoption of self-driving vehicles that are dependent on AI sensors like cameras, LiDAR, and radar. The United States has experienced a rise in the adoption of these sensors in the majority of healthcare applications like diagnostics, medical imaging, and patient monitoring.

Europe is projected to lead as the second leading region in the market owing to factors like government support, the adoption of smart manufacturing, and the rise of smart cities. Europe has been leading in backing research and development of AI.

Moreover, the European Commission has highlighted AI with funding initiatives like Horizon Europe that backs innovations in AI. The region also leads in Industry 4.0 and smart manufacturing, which are largely dependent on AI sensors for real-time monitoring, automation, and predictive maintenance in most industries.

In addition, Europe has witnessed substantial growth in healthcare sectors and smart cities, where AI sensors are increasingly used in energy optimization, traffic management, and medical diagnostics.

Competitive Analysis

The global artificial intelligence (AI) sensors market is led by players like:

- Nvidia Corporation

- Intel Corporation

- Texas Instruments

- Honeywell International Inc.

- Bosch Sensortec GmbH

- STMicroelectronics

- Qualcomm Technologies Inc.

- Analog Devices Inc.

- Infineon Technologies AG

- Renesas Electronics Corporation

- Omron Corporation

- Xilinx Inc.

- Toshiba Corporation

- Flir Systems Inc.

- Sony Corporation

Key Market Trends

- Integration with smart homes and IoT:

Smart home automation and IoT are among the leading drivers of the rise of AI sensors. These sensors in smart technologies, security devices, and lighting systems are improving user experience by allowing smart and data-based automation and decision-making.

- AI Sensors in healthcare for monitoring systems and diagnostics:

AI sensors are widely integrated in the healthcare sector for uses like diagnostic systems, medical imaging, and remote patient monitoring. They aid in early disease detection, supporting personalized treatments, and enhancing the accuracy of diagnostics.

The global artificial intelligence (AI) sensors market is segmented as follows:

By Type

- Pressure

- Temperature

- Optical

- Position

- Ultrasonic

- Motion

- Navigation

- Others

By Technology

- NLP

- Machine Learning

- Computer Vision

By Application

- Automotive

- Consumer Electronics

- Manufacturing

- Aerospace and Defense

- Robotics

- Smart Home Automation

- Others

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Nvidia Corporation

- Intel Corporation

- Texas Instruments

- Honeywell International Inc.

- Bosch Sensortec GmbH

- STMicroelectronics

- Qualcomm Technologies Inc.

- Analog Devices Inc.

- Infineon Technologies AG

- Renesas Electronics Corporation

- Omron Corporation

- Xilinx Inc.

- Toshiba Corporation

- Flir Systems Inc.

- Sony Corporation

Frequently Asked Questions

Copyright © 2024 - 2025, All Rights Reserved, Facts and Factors