![]()

Search Market Research Report

Automated Cell Counters Market

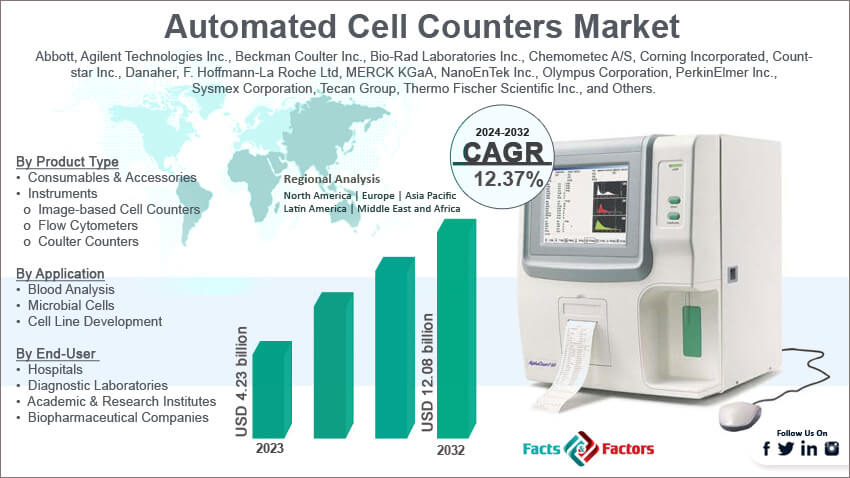

Automated Cell Counters Market Size, Share, Growth Analysis Report By Product Type (Consumables & Accessories and Instruments), By Application (Blood Analysis, Microbial Cells, Cell Line Development, and Others), By End-User (Hospitals, Diagnostic Laboratories, Academic & Research Institutes, Biopharmaceutical Companies, and Others), and By Region - Global and Regional Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2024 – 2032

Industry Insights

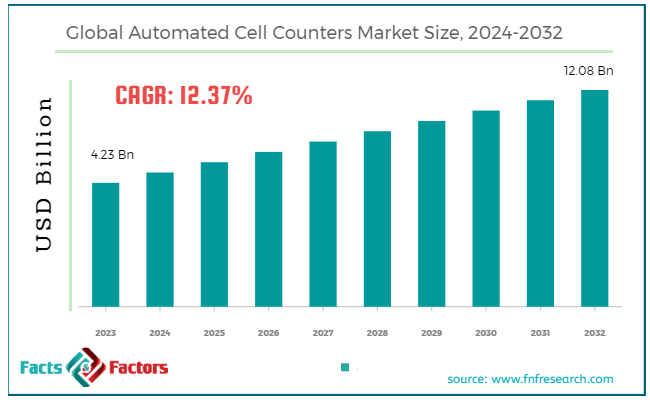

[222+ Pages Report] According to Facts & Factors, the global automated cell counters market size in terms of revenue was valued at around USD 4.23 billion in 2023 and is expected to reach a value of USD 12.08 billion by 2032, growing at a CAGR of roughly 12.37% from 2024 to 2032. The global automated cell counters market is projected to grow at a significant growth rate due to several driving factors.

Market Overview

Market Overview

Automated cell counters are advanced laboratory instruments designed to count and analyze cells in a sample quickly and accurately. These devices are essential in various fields, including clinical diagnostics, pharmaceutical research, biotechnology, and academic research. Automated cell counters use different technologies such as flow cytometry, image analysis, and electrical impedance to determine cell concentration, viability, and other characteristics.

The automated cell counters market is expanding rapidly, driven by the increasing demand for accurate and efficient cell analysis in research and clinical diagnostics. The market's growth is also propelled by technological advancements, the rising prevalence of chronic diseases, and the growing adoption of automated systems in laboratories to enhance productivity and precision.

Key Highlights

- The automated cell counters market has registered a CAGR of 12.37% during the forecast period.

- In terms of revenue, the global automated cell counters market was estimated at roughly USD 4.23 billion in 2023 and is predicted to attain a value of USD 12.08 billion by 2032.

- The automated cell counters market is poised for substantial growth, driven by technological advancements, increasing prevalence of chronic diseases, and growing adoption in research and biotechnology.

- Based on the product type, the consumables & accessories segment is growing at a high rate and is projected to dominate the global market.

- On the basis of application, the cell line development segment is projected to swipe the largest market share.

- Based on the end-user, the biopharmaceutical companies segment is expected to dominate the global market.

- By region, North America dominates the automated cell counters market due to the presence of advanced healthcare infrastructure, adoption of hi-tech innovations, and significant investment in R&D.

Growth Drivers:

- Rising Prevalence of Chronic Diseases: The growing burden of chronic illnesses like cancer and blood disorders necessitates faster and more accurate cell analysis, propelling the adoption of automated cell counters.

- Increased Research & Development Activities: The surge in research activities across pharmaceuticals, biotechnology, and life sciences is fueling the demand for automated cell counting solutions for drug discovery, cell line development, and other applications.

- Improved Accuracy & Efficiency: Advancements in automation, digital imaging, and flow cytometry technologies are leading to more accurate and efficient cell counting compared to traditional manual methods.

- Growing Focus on Personalized Medicine: The rise of personalized medicine approaches that tailor treatments based on individual patients' cell characteristics creates a need for faster and more precise cell analysis tools.

- Convenience & Ease of Use: Automated cell counters offer user-friendly interfaces and streamlined workflows, making them accessible to a wider range of researchers and technicians, even those with less experience in manual cell counting.

Restraints:

- High Initial Investment Costs: The initial cost of acquiring automated cell counters can be high, particularly for sophisticated instruments with advanced features. This can be a barrier for smaller labs and research institutions with limited budgets.

- Limited Availability of Skilled Personnel: Operating and interpreting data from some automated cell counters may require specialized training or expertise, which can be a challenge for some labs.

- Data Security Concerns: Storing and managing large amounts of cell count data electronically raises concerns about data security and privacy breaches.

Opportunities:

- Development of Cost-Effective Solutions: Manufacturers focusing on developing more affordable automated cell counters with essential functionalities can expand market penetration to cost-conscious labs.

- Emerging Markets & Decentralized Labs: Growing research activities in emerging markets and the increasing trend of establishing smaller, decentralized labs create opportunities for portable and user-friendly automated cell counters.

- Integration with Artificial Intelligence (AI): Incorporating AI algorithms for automated cell classification and data analysis can enhance the accuracy and efficiency of automated cell counters, attracting new users.

- Focus on Multifunctionality: Developing automated cell counters that can perform multiple functions, such as cell counting, viability analysis, and cell size measurement, can offer greater value to researchers.

Challenges:

- Regulatory Landscape: Evolving regulations around medical device approvals and data privacy can pose challenges for manufacturers entering new markets or developing innovative technologies.

- Competition: The automated cell counter market is becoming increasingly competitive, with established players and new entrants vying for market share. This can lead to pressure on pricing and profit margins.

- Standardization & Interoperability: Lack of standardization in data formats and communication protocols across different automated cell counter models can create challenges for data sharing and integration with existing laboratory workflows.

Automated Cell Counters Market: Segmentation Analysis

The global automated cell counters market is segmented based on product type, application, end-user, and region.

By Product Type Insights

Based on Product Type, the global automated cell counters market is divided into consumables & accessories and instruments. The consumables and accessories segment held the largest market share in 2023 and is expected to grow fastest CAGR over the forecast period. Consumables and accessories are essential components of automated cell counters, including reagents, test kits, slides, tubes, and other disposable items used in cell counting procedures. These products are necessary for the routine operation and maintenance of cell counters, ensuring accuracy and reliability in results. The consumables and accessories segment is driven by the increasing adoption of automated cell counters across various applications such as medical diagnostics, research, and pharmaceuticals. The recurring need for consumables in every test cycle ensures a steady demand.

The instruments segment is expected to grow robustly. Instruments in the automated cell counters market include the actual devices used for counting cells, such as hematology analyzers, flow cytometers, fluorescence image-based cell counters, Coulter counters, and spectrophotometers. These instruments are critical for performing precise and accurate cell counting in medical diagnostics, research, and drug discovery. The instruments segment is driven by technological advancements that enhance the capabilities and efficiency of automated cell counters. The rising prevalence of chronic diseases and the growing need for early and accurate diagnosis are also significant factors driving the demand for advanced cell counting instruments.

By Application Insights

On the basis of Application, the global automated cell counters market is bifurcated into blood analysis, microbial cells, cell line development, and others. Blood analysis is one of the primary applications of automated cell counters, involving the quantification and analysis of different blood cell types. This application is crucial for diagnosing and monitoring various blood-related disorders and diseases. The demand for automated cell counters in blood analysis is driven by the increasing prevalence of blood disorders such as anemia, leukemia, and thalassemia. These instruments provide quick, accurate, and detailed information about blood cells, essential for effective diagnosis and treatment. The growing aging population, which is more susceptible to blood disorders, further boosts the demand for automated cell counters in this application.

Microbial Cells segment using automated cell counters is vital in various fields, including microbiology, biotechnology, and pharmaceuticals. This application involves counting and characterizing bacterial, fungal, and other microbial cells. The demand for automated cell counters in microbial cell analysis is driven by the need for accurate and efficient microbial quantification in research and clinical settings. In the pharmaceutical industry, microbial cell counting is crucial for drug development and quality control.

The cell line development segment accounted for 32.2% of revenue share in 2023. The cell Line development segment creates stable cell lines that can be used for various applications in research, drug discovery, and bioproduction. Automated cell counters are essential for monitoring cell growth, viability, and density during this process. The demand for automated cell counters in cell line development is driven by the growing biopharmaceutical industry and the increasing focus on biologics and personalized medicine. Automated cell counters provide accurate and real-time monitoring of cell cultures, which is crucial for optimizing cell line development and ensuring reproducibility.

By End-User Insights

Based on End-User, the global automated cell counters market is categorized into hospitals, diagnostic laboratories, academic & research institutes, biopharmaceutical companies, and others. Hospitals are one of the primary end-users of automated cell counters, utilizing these devices for various diagnostic purposes. Automated cell counters in hospitals are crucial for analyzing blood samples, diagnosing hematological disorders, and monitoring patient health. The demand for automated cell counters in hospitals is driven by the need for accurate and rapid diagnostic results. The increasing prevalence of chronic diseases such as cancer, diabetes, and cardiovascular conditions requires frequent blood analysis, further boosting the demand.

Diagnostic laboratories are major users of automated cell counters, employing these devices for a wide range of tests, including blood analysis, microbial cell counting, and other specialized assays. These labs provide essential diagnostic services to hospitals, clinics, and individual patients. The growth in the diagnostic laboratories segment is driven by the increasing demand for comprehensive diagnostic services and the need for high-throughput and precise cell counting technologies.

Academic and research institutes utilize automated cell counters for various research applications, including cellular biology, cancer research, immunology, and drug discovery. These institutions require accurate cell counting for experimental reproducibility and data accuracy. The demand for automated cell counters in academic and research institutes is driven by the increasing focus on advanced biomedical research and the need for precise cell quantification.

The biopharmaceutical companies segment is expected to dominate the global market during the forecast period. Biopharmaceutical companies are key users of automated cell counters, employing these devices for various applications, including drug development, quality control, and manufacturing processes. Automated cell counters help ensure the consistency and quality of biopharmaceutical products. The growth in the biopharmaceutical companies segment is driven by the increasing investment in biopharmaceutical research and the development of new biologic drugs.

Recent Developments:

- (October 2023): The DeNovix CellDrop Automated Cell Counter becomes the first of its kind to receive ACT Label certification for environmental sustainability through My Green Lab. This recognition highlights the growing focus on eco-friendly solutions in the life sciences industry.

- (January 2023): Thermo Fisher Scientific introduces the Big Foot cell sorter to the Indian market. This user-friendly instrument boasts a tenfold speed increase compared to existing cell sorting solutions, accelerating research and development activities.

- (March 2022): Erasmus MC in the Netherlands partners with Sectra to implement a digital pathology system. This collaboration allows pathologists to analyze and collaborate on cases remotely, exceeding the capabilities of traditional microscopy. This shift promises improved efficiency and reduced variability in diagnoses, potentially leading to better cancer care in the future.

Report Scope

Report Attribute |

Details |

Market Size in 2023 |

USD 4.23 Billion |

Projected Market Size in 2032 |

USD 12.08 Billion |

CAGR Growth Rate |

12.37% CAGR |

Base Year |

2023 |

Forecast Years |

2024-2032 |

Key Market Players |

Abbott, Agilent Technologies Inc., Beckman Coulter Inc., Bio-Rad Laboratories Inc., Chemometec A/S, Corning Incorporated, Countstar Inc., Danaher, F. Hoffmann-La Roche Ltd, MERCK KGaA, NanoEnTek Inc., Olympus Corporation, PerkinElmer Inc., Sysmex Corporation, Tecan Group, Thermo Fischer Scientific Inc., and Others. |

Key Segment |

By Product Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Automated Cell Counters Market: Regional Analysis

- North America led the global market

North America holds the largest share of over 38.4% in 2023, attributed to its advanced healthcare infrastructure, substantial investments in research and development, and the presence of major manufacturers. The United States, in particular, leads this market due to strong R&D capabilities and a high concentration of leading biotechnology and pharmaceutical companies such as Thermo Fisher Scientific, Bio-Rad Laboratories, and Agilent Technologies. The demand for early diagnostic procedures and the high prevalence of chronic diseases further boost the market.

In Europe, the market is driven by increasing investments in biopharmaceutical research, the adoption of advanced medical technologies, and efforts to address medical staff shortages. Countries such as Germany, the UK, and France are at the forefront, leading in the adoption of automated cell counting technologies. The European market benefits from favorable regulatory policies promoting advanced medical practices and significant investments in genomics, proteomics, and stem cell research. This region's market is projected to grow steadily due to ongoing technological advancements and substantial research investments.

The Asia-Pacific region is witnessing the fastest growth in the automated cell counters market, with countries like China, Japan, and India driving this expansion. In 2023, Japan holds the largest share in the Asia Pacific. Significant investments in healthcare infrastructure, advancements in medical technology, and increasing research activities are key factors. The growing elderly population and rising incidence of chronic diseases further contribute to market growth. Additionally, the trend of medical tourism and the affordability of diagnostic procedures in countries like China and India attract global patients, bolstering the market.

Latin America is emerging as a significant market for automated cell counters, with notable growth in countries like Brazil. The region's expansion is driven by increasing healthcare investments, rising awareness about advanced diagnostic technologies, and a growing demand for improved healthcare services. Economic development and improving healthcare access are also contributing to market growth.

In the Middle East & Africa, the automated cell counters market is gradually expanding. Efforts to modernize healthcare infrastructure and increase investments in research and development are driving market growth. Countries such as the UAE and South Africa are leading in the adoption of advanced medical technologies. Government initiatives to enhance healthcare and research capabilities, coupled with a growing need for advanced diagnostic tools to manage chronic diseases, support the market's steady growth.

Automated Cell Counters Market: Competitive Landscape

Some of the main competitors dominating the global automated cell counters market include;

- Abbott

- Agilent Technologies, Inc.

- Beckman Coulter Inc.

- Bio-Rad Laboratories, Inc.

- Chemometec A/S

- Corning Incorporated

- Countstar, Inc.

- Danaher

- F. Hoffmann-La Roche Ltd

- MERCK KGaA

- NanoEnTek Inc.

- Olympus Corporation

- PerkinElmer Inc.

- Sysmex Corporation

- Tecan Group

- Thermo Fischer Scientific Inc.

The global automated cell counters market is segmented as follows:

By Product Type Segment Analysis

- Consumables & Accessories

- Instruments

- Image-based Cell Counters

- Flow Cytometers

- Coulter Counters

By Application Segment Analysis

- Blood Analysis

- Microbial Cells

- Cell Line Development

- Others

By End-User Segment Analysis

- Hospitals

- Diagnostic Laboratories

- Academic & Research Institutes

- Biopharmaceutical Companies

- Others

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Abbott

- Agilent Technologies, Inc.

- Beckman Coulter Inc.

- Bio-Rad Laboratories, Inc.

- Chemometec A/S

- Corning Incorporated

- Countstar, Inc.

- Danaher

- F. Hoffmann-La Roche Ltd

- MERCK KGaA

- NanoEnTek Inc.

- Olympus Corporation

- PerkinElmer Inc.

- Sysmex Corporation

- Tecan Group

- Thermo Fischer Scientific Inc.

Frequently Asked Questions

Copyright © 2024 - 2025, All Rights Reserved, Facts and Factors