![]()

Search Market Research Report

Solar Panel Cleaning Market Size, Share Global Analysis Report, 2024 – 2032

Solar Panel Cleaning Market Size, Share, Growth Analysis Report By Mode of Operation (Manual and Autonomous), By Process (Automated, Semi-Automated, Automated Robotic, Water Brushes, Electrostatic, and Others), By Technology (Wet Cleaning and Dry Cleaning), By Application (Commercial, Residential, and Industrial & Utility), And By Region - Global and Regional Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2024 – 2032

Industry Insights

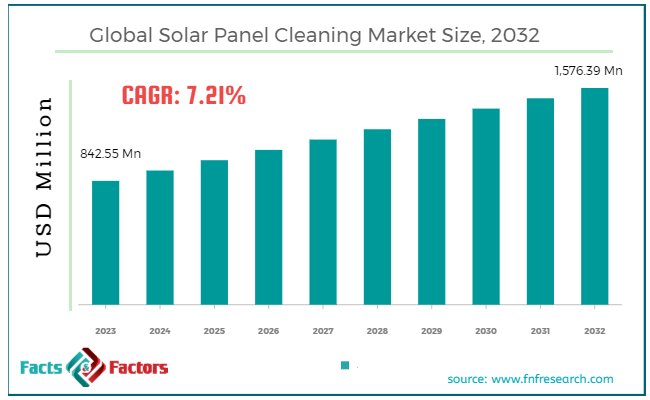

[221+ Pages Report] According to Facts & Factors, the global solar panel cleaning market size in terms of revenue was valued at around USD 842.55 million in 2023 and is expected to reach a value of USD 1,576.39 million by 2032, growing at a CAGR of roughly 7.21% from 2024 to 2032. The global solar panel cleaning market is projected to grow at a significant growth rate due to several driving factors.

Market Overview

Market Overview

Solar panel cleaning involves the removal of dirt, dust, pollen, bird droppings, and other debris from the surface of solar photovoltaic (PV) panels. This is essential because such residues can significantly reduce the efficiency of solar panels by blocking sunlight and diminishing their energy output. Over time, accumulated dirt can lead to a decrease in electrical output, sometimes by as much as 20% to 30%, which impacts the overall performance and efficiency of the solar energy system.

The cleaning process can be done manually using brushes and squeegees or through automated systems such as robotic cleaners and sprinkler-like cleaning systems. The frequency and method of cleaning depend on several factors including the location of the panels, local weather conditions, and the level of airborne dust and debris. In areas with high dust levels or frequent bird activity, more regular cleaning may be necessary. Ensuring that solar panels are clean not only maximizes their energy production but also extends their lifespan by preventing long-term damage from dirt accumulation and environmental wear and tear.

Key Highlights

- The solar panel cleaning market has registered a CAGR of 7.21% during the forecast period.

- In terms of revenue, the global solar panel cleaning market was estimated at roughly USD 842.55 million in 2023 and is predicted to attain a value of USD 1,576.39 million by 2032.

- The expansion of the solar panel cleaning market is driven by the increasing number of solar panel installations, the recognition of the efficiency decline caused by dirt accumulation, and the progress in cleaning solutions technology.

- On the basis of mode of operation, the autonomous segment is projected to swipe the largest market share.

- In terms of process, the automated robotic segment is expected to witness significant growth, driven by breakthroughs in robotics technology and the growing affordability of robotic systems.

- Based on the application, the industrial & utility segment is growing at a high rate and is projected to dominate the global market.

- Asia-Pacific region will dominate the global solar panel cleaning market.

Growth Drivers:

- Surging Solar Panel Installations: The rapid rise of solar power installations globally creates a significant demand for regular panel cleaning to maintain optimal performance. As more homes and businesses harness the sun's energy, the market for cleaning services expands.

- Awareness of Efficiency Loss Due to Soiling: Growing awareness of the impact of dust and grime on solar panel efficiency is prompting owners to prioritize cleaning. This understanding translates to a rise in demand for professional cleaning services or investment in proper cleaning equipment for self-maintenance.

- Stringent Environmental Regulations: Some regions are implementing stricter regulations regarding dust emissions from solar farms. Regular cleaning ensures compliance with these regulations, driving the market for cleaning solutions.

- Technological Advancements in Cleaning Solutions: Development of innovative cleaning robots and drones specifically designed for solar panels offers efficient and cost-effective cleaning options. These advancements contribute to market growth by making professional cleaning more accessible.

Restraints:

- Cost Considerations: The cost of professional cleaning services can be a deterrent for some solar panel owners, particularly for smaller residential systems. This can lead to a preference for self-cleaning or delaying cleaning altogether, impacting overall market growth.

- Water Scarcity Concerns: In regions with water scarcity, traditional water-based cleaning methods might not be sustainable. Developing and adopting water-saving cleaning techniques or alternative cleaning solutions are crucial to overcome this restraint.

- Limited Awareness in Certain Regions: In areas with a relatively new solar energy sector, awareness about the importance of regular cleaning and its impact on efficiency might be low. Educational initiatives are needed to address this gap and promote a culture of proper solar panel maintenance.

Opportunities:

- Focus on Sustainability: Developing eco-friendly cleaning solutions and water-saving cleaning techniques presents a significant opportunity for market growth. This caters to the growing demand for sustainable practices within the solar energy sector.

- Subscription-Based Cleaning Services: Subscription-based cleaning services offer a convenient and cost-effective way for solar panel owners to ensure regular maintenance. This model presents an opportunity to attract new customers and build long-term relationships.

- Expansion into Emerging Markets: The increasing adoption of solar power in developing countries creates new market opportunities for solar panel cleaning services. Adapting existing service models and pricing structures to these emerging markets can be a significant growth driver.

Challenges:

- Safety Concerns: Cleaning solar panels, especially on rooftops or large installations, can be risky. Developing and implementing proper safety protocols for cleaning staff is essential to ensure a safe working environment.

- Standardization of Cleaning Practices: The lack of standardized cleaning procedures across the industry can lead to inconsistent results and potential damage to panels. Establishing industry-wide cleaning standards would benefit both service providers and solar panel owners.

- Diverse Environmental Conditions: Weather conditions can limit the effectiveness and frequency of cleaning. Developing cleaning solutions that are less weather-dependent or exploring alternative cleaning methods can help overcome this challenge.

Solar Panel Cleaning Market: Segmentation Analysis

The global solar panel cleaning market is segmented based on mode of operation, process, technology, application, and region.

By Mode of Operation Insights

Based on Mode of Operation, the global solar panel cleaning market is divided into manual and autonomous. Manual cleaning involves human labor to physically clean the solar panels using brushes, squeegees, and cleaning solutions. This method is often used in smaller installations or in regions where labor costs are low. The manual cleaning segment benefits from its simplicity and low initial cost since it doesn't require sophisticated equipment. However, it can be labor-intensive and less efficient for large-scale solar farms. Manual cleaning is more common in developing regions and in residential or small commercial settings where the scale of solar installations does not justify the high cost of automated systems.

Autonomous or automated cleaning includes the use of robotic systems and other automated technologies to clean solar panels without human intervention. These systems may use brushes, air jets, or other mechanisms to remove dirt and debris from the solar panels. The autonomous cleaning segment is growing rapidly, driven by the need for efficient and cost-effective solutions in large-scale solar installations.

These systems reduce the need for manual labor, minimize water usage, and can operate without human intervention, making them ideal for utility-scale solar parks. Technological advancements and the decreasing cost of robotics are making autonomous systems increasingly accessible and economically viable, especially in developed markets with higher labor costs.

The autonomous segment is expected to exhibit a higher CAGR compared to manual cleaning, due to increasing investments in technology and a growing preference for labor-saving and environmentally friendly cleaning solutions across major solar markets. The trend towards automation is particularly strong in regions with large solar farms and where efficiency and minimal operational disruption are priorities.

By Process Insights

On the basis of Process, the global solar panel cleaning market is bifurcated into automated, semi-automated, automated robotic, water brushes, electrostatic, and others. Automated cleaning systems operate without manual intervention, often using sophisticated mechanisms and sensors to clean panels efficiently. The automated segment is expected to exhibit a high CAGR. This segment is favored for large-scale solar installations due to its efficiency and ability to reduce labor costs significantly.

Semi-automated systems require some human intervention or supervision but utilize machinery to assist in the cleaning process, such as motorized brushes or controlled spray mechanisms. The semi-automated segment shows moderate growth potential. This segment offers a balance between cost and efficiency, making it suitable for medium-scale installations or regions where full automation is not economically viable. It's a transitional solution that caters to markets gradually shifting from manual to fully automated solutions.

Automated Robotic systems use robots designed specifically for solar panel cleaning, which can navigate the layout of solar arrays autonomously, often equipped with sensors to detect dirt levels and optimize the cleaning cycle. The rapid advancement in robotics and AI has propelled this segment, especially in markets with high labor costs and large photovoltaic (PV) installations. The precision and adaptability of these robots can significantly enhance cleaning efficacy and are increasingly becoming a popular choice. This segment is likely to experience one of the highest CAGRs among the categories.

Water brushes use soft brushes and water to gently remove dirt from the surface of solar panels, often mounted on an automated system that moves along the rows of panels. While effective, the reliance on water can be a drawback in areas with water scarcity. However, this method is still prevalent in regions with adequate water resources and where minimal abrasion is crucial.

Electrostatic cleaning systems use static electricity to repel dust and dirt from solar panels without physical contact or water, making it highly suitable for dry and dusty environments. This technology is relatively new but is gaining traction due to its minimal water use and the ability to maintain panel efficiency in arid climates where water-based cleaning methods are not feasible.

By Technology Insights

Based on Technology, the global solar panel cleaning market is categorized into wet cleaning and dry cleaning. Wet cleaning involves using water, often with detergents or other cleaning agents, to remove dirt and debris from solar panels. This method may employ manual sponging or brushing, or more commonly, automated systems that spray water and scrub the panels.

Wet cleaning is highly effective at removing stubborn dirt and is widely used where water availability is not a concern. The technique is particularly prevalent in regions with frequent rainfall, which naturally helps reduce the frequency of required cleanings. However, the use of water raises concerns in areas prone to drought or where water conservation is prioritized. The CAGR for the wet cleaning segment is robust but may be moderated.

Dry cleaning methods include using brushes, air jets, or electrostatic technologies to clean solar panels without water. These methods are advantageous in regions with water use restrictions or in environments where water could freeze, damaging the panels. Dry cleaning is gaining popularity due to its minimal environmental impact and its applicability in diverse climates, including very cold or very dry areas. The development of advanced dry cleaning technologies, such as robotic brushes and electrostatic systems, enhances the efficiency and effectiveness of these methods. The dry cleaning segment is expected to see significant growth, potentially experiencing a higher CAGR than wet cleaning.

By Application Insights

In terms of Application, the global solar panel cleaning market is divided into commercial, residential, and industrial & utility. Commercial segment includes solar panel installations at commercial properties, such as office buildings, shopping centers, and schools. These installations are typically of moderate size but are often located in accessible areas, making regular maintenance feasible.

The commercial sector often opts for regular cleaning services to maintain the aesthetic appeal of the buildings and ensure optimal energy efficiency. The growing adoption of green energy solutions in the commercial sector drives the demand for professional cleaning services that can provide both efficiency and convenience. The CAGR for the commercial segment is steady.

Residential solar panel cleaning pertains to smaller-scale installations typically found on individual homes. These systems may require less frequent cleaning compared to commercial and industrial setups. Property-owners are becoming more aware of the efficiency losses due to dirty solar panels, driving demand for cleaning services.

However, the decision to invest in professional cleaning can depend significantly on local climate conditions and the homeowner’s awareness of solar efficiency issues. The residential segment is expected to grow at a moderate pace. The market expansion is somewhat tempered by the variability in homeowners’ willingness to pay for professional cleaning services, but overall growth is supported by the increasing adoption of residential solar systems.

Industrial & Utility segment covers large-scale solar installations used in industrial applications and utility-scale solar farms. The industrial & utility segment is likely to witness the highest CAGR among the application. These installations are often in expansive, sometimes remote areas and can encompass thousands of solar panels. Given the scale of these installations and the significant revenue implications of any efficiency losses, regular and highly efficient cleaning is crucial. The industrial and utility segment often employs automated and robotic cleaning systems to handle the vast areas covered by solar arrays efficiently.

Report Scope

Report Attribute |

Details |

Market Size in 2023 |

USD 842.55 Million |

Projected Market Size in 2032 |

USD 1,576.39 Million |

CAGR Growth Rate |

7.21% CAGR |

Base Year |

2023 |

Forecast Years |

2024-2032 |

Key Market Players |

BladeRanger, Boson Robotics Ltd., Clean Solar Solutions, Ecoppia, Ecovacs Robotics, Heliotex, Indisolar Products Private Limited, Karcher, kärcher türkiye, Kashgar Solbright Photovoltaic Technology Co. Ltd., Nomadd, Parish Maintenance Supply, Premier Solar Cleaning LLC, Saint-Gobain, Serbot AG, Sharp Corporation, Solar Cleaning Machinery, SunBrush Mobil GmbH, and Others. |

Key Segment |

By Mode of Operation, By Process, By Technology, By Application, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Solar Panel Cleaning Market: Regional Analysis

- Asia-Pacific likely to experience the fastest growth from 2024 to 2032

The Asia-Pacific region is rapidly becoming the fastest-growing market for solar panel cleaning, with a CAGR that could exceed 20.78%. Asia Pacific is a solar energy powerhouse, with countries like China and India leading the charge. This surge in solar installations translates to a massive demand for regular panel cleaning to maintain optimal efficiency.

Some Asian governments are providing subsidies or incentives for solar panel cleaning services, further propelling market growth. This highlights the growing recognition of the importance of panel maintenance for maximizing solar energy generation. The presence of vast solar farms in Asia Pacific creates a need for specialized cleaning solutions and potentially higher service volumes compared to regions dominated by rooftop installations.

In North America, the United States leads in solar panel installations, and consequently, in the solar panel cleaning market. This is due to the large scale of solar farms as well as numerous residential and commercial solar setups. Companies in this region are increasingly adopting automated solar panel cleaning systems to enhance efficiency and reduce labor costs, reflecting a CAGR that is expected to be robust, potentially in the range of 10.15% over the next few years. Factors contributing to this growth include technological advancements in cleaning equipment, a strong push towards maximizing energy efficiency of solar installations, and supportive state-level policies promoting solar energy adoption.

Europe continues to exhibit strong market growth, driven by stringent EU regulations on renewable energy and sustainability. Germany, Spain, and Italy, in particular, have significant installed solar capacities, which necessitate efficient maintenance solutions. The European market is likely to have a CAGR similar to or slightly higher than North America, estimated at around 12.17%, facilitated by high adoption rates of innovative and eco-friendly cleaning technologies, including robotic and water-less cleaning systems.

The Middle East & Africa region presents a unique market with high potential for solar panel cleaning due to its geographic and climatic conditions that lead to quick accumulation of dust and debris on panels. While the market is still developing, countries like Saudi Arabia, the UAE, and South Africa are investing in solar energy infrastructure, which in turn drives the need for effective cleaning solutions. The CAGR in this region is expected to grow significantly, though from a smaller base, potentially around 15.24% in the coming years.

Latin America’s solar panel cleaning market is nascent but shows promise with countries like Brazil, Mexico, and Chile leading in solar adoption. The market's growth is driven by increased local and foreign investments in solar energy. The CAGR in this region is expected to be competitive, potentially around 10-15%, as more structured and efficient cleaning services begin to penetrate the market.

Solar Panel Cleaning Market: Competitive Landscape

Some of the main competitors dominating the global solar panel cleaning market include;

- BladeRanger

- Boson Robotics Ltd.

- Clean Solar Solutions

- Ecoppia

- Ecovacs Robotics

- Heliotex

- Indisolar Products Private Limited

- Karcher

- kärcher türkiye

- Kashgar Solbright Photovoltaic Technology Co. Ltd.

- Nomadd

- Parish Maintenance Supply

- Premier Solar Cleaning, LLC

- Saint-Gobain

- Serbot AG

- Sharp Corporation

- Solar Cleaning Machinery

- SunBrush Mobil GmbH

The global solar panel cleaning market is segmented as follows:

By Mode of Operation Segment Analysis

- Manual

- Autonomous

By Process Segment Analysis

- Automated

- Semi-Automated

- Automated Robotic

- Water Brushes

- Electrostatic

- Others

By Technology Segment Analysis

- Wet Cleaning

- Dry Cleaning

By Application Segment Analysis

- Commercial

- Residential

- Industrial & Utility

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- BladeRanger

- Boson Robotics Ltd.

- Clean Solar Solutions

- Ecoppia

- Ecovacs Robotics

- Heliotex

- Indisolar Products Private Limited

- Karcher

- kärcher türkiye

- Kashgar Solbright Photovoltaic Technology Co. Ltd.

- Nomadd

- Parish Maintenance Supply

- Premier Solar Cleaning, LLC

- Saint-Gobain

- Serbot AG

- Sharp Corporation

- Solar Cleaning Machinery

- SunBrush Mobil GmbH

Frequently Asked Questions

Copyright © 2024 - 2025, All Rights Reserved, Facts and Factors