![]()

Search Market Research Report

India Telehealth Services Market

India Telehealth Services Market Size, Share, Growth Analysis Report By Component (Hardware, Software, and Services), By Type (Telemedicine, e-Consultation, Tele-Hospitals, and mHealth), By Application (Teleradiology, Telepsychiatry, Teledermatology, Telepathology, Telecardiology, Teleconsultation, and Others), By End-User (Providers, Patients, and Others), and By Region - Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2024 – 2032

Industry Insights

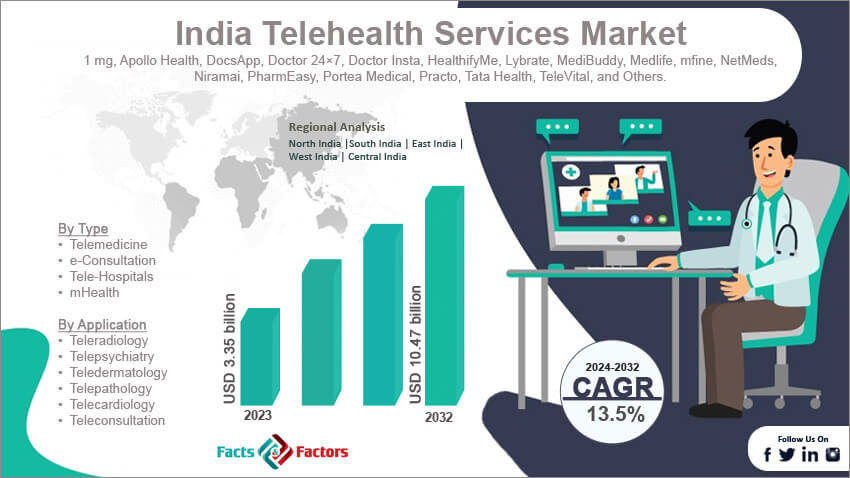

[219+ Pages Report] According to Facts & Factors, the India telehealth services market size in terms of revenue was valued at around USD 3.35 billion in 2023 and is expected to reach a value of USD 10.47 billion by 2032, growing at a CAGR of roughly 13.5% from 2024 to 2032. The India telehealth services market is projected to grow at a significant growth rate due to several driving factors.

Market Overview

Market Overview

India telehealth services refer to the use of digital and telecommunication technologies to deliver healthcare services remotely. These services encompass a wide range of applications, including virtual consultations, remote monitoring, telemedicine, and digital health platforms. Telehealth enables healthcare providers to offer medical advice, diagnose conditions, and manage treatments without the need for physical visits, thereby improving access to healthcare, especially in rural and underserved areas. The India telehealth services market has experienced significant growth, driven by factors such as increasing internet penetration, rising smartphone usage, and the growing demand for convenient and accessible healthcare solutions.

Additionally, the COVID-19 pandemic has accelerated the adoption of telehealth services as people seek safer alternatives to in-person consultations. Government initiatives and supportive policies to promote digital health further boost the market. As a result, the India telehealth services market is poised for continued expansion, driven by technological advancements, evolving consumer preferences, and the need for efficient healthcare delivery systems.

Key Highlights

- The India telehealth services market has registered a CAGR of 13.5% during the forecast period.

- In terms of revenue, the India telehealth services market was estimated at roughly USD 3.35 billion in 2023 and is predicted to attain a value of USD 10.47billion by 2032.

- The diverse regional dynamics reflect varying levels of development, healthcare access, and technological adoption across India, contributing to the overall expansion of the telehealth services market.

- On the basis of component, the services segment is growing at a high rate and is projected to dominate the market.

- In terms of application, the telepsychiatry segment is expected to dominate the market.

- By region, South India is expected to dominate the market during the forecast period.

Growth Drivers:

- Rising Healthcare Costs: Telehealth offers a cost-effective alternative to traditional in-person consultations, making healthcare more accessible to a wider population.

- Increasing Internet and Smartphone Penetration: Improved Internet connectivity and smartphone affordability are crucial for facilitating telehealth services across the country.

- Growing Awareness and Acceptance: The COVID-19 pandemic significantly boosted awareness and acceptance of telehealth consultations, paving the way for its wider adoption.

- Government Support: Government initiatives promoting telemedicine and digital healthcare infrastructure creation further fuel market growth.

- Shortage of Qualified Medical Professionals: Telehealth helps bridge the gap in geographically remote areas with limited access to qualified healthcare professionals.

Restraints:

- Limited Infrastructure and Connectivity: Uneven internet penetration, particularly in rural areas, can hinder access to telehealth services.

- Data Privacy and Security Concerns: Ensuring robust data security measures and patient privacy is crucial for building trust in telehealth platforms.

- Regulatory Hurdles: Evolving regulations and legal frameworks surrounding telehealth practices need to be streamlined for smooth operation.

- Lack of Reimbursement Parity: Limited insurance coverage for telehealth consultations can be a barrier for some patients.

- Digital Literacy Gap: A segment of the population, particularly the elderly, may lack the digital literacy required to utilize telehealth services effectively.

Opportunities:

- Focus on Speciality Telehealth Services: Expanding telehealth services beyond general consultations to include specialized consultations can cater to a wider range of healthcare needs.

- Integration with Artificial Intelligence: Incorporating AI-powered chatbots and symptom checkers can enhance patient experience and offer preliminary diagnoses.

- Mobile Health Apps and Wearable Devices: Leveraging mobile health apps and wearable devices for remote patient monitoring and data collection can offer valuable insights for healthcare providers.

- Rural Outreach Programs: Targeted outreach programs can bridge the digital divide and create awareness about telehealth services in rural areas.

- Collaboration between Public and Private Sectors: Collaboration between public and private healthcare providers can optimize resource allocation and expand the reach of telehealth services.

Challenges:

- Standardization and Quality Control: Ensuring standardized practices and maintaining quality of care across different telehealth platforms is crucial.

- Cybersecurity Threats: Robust cybersecurity measures are essential to protect sensitive patient data from cyberattacks and breaches.

- Physician Training and Adoption: Encouraging healthcare professionals to adopt telehealth practices and undergo necessary training is vital for successful implementation.

Segmentation Analysis

The India telehealth services market is segmented based on component, type, application, end-user, and region.

- By Component Insights

Based on Component, the India telehealth services market is divided into hardware, software, and services.

The hardware segment includes physical devices and equipment used in telehealth services. This comprises telemedicine carts, kiosks, digital diagnostic, wearable devices, and communication infrastructure. The hardware segment is driven by the increasing adoption of advanced medical devices and the need for reliable communication tools to facilitate remote consultations. As telehealth services expand, there is a growing demand for high-quality hardware to ensure accurate diagnostics and effective patient monitoring.

The software segment encompasses the digital platforms and applications used to deliver telehealth services. This includes telemedicine software, electronic health records (EHR) systems, patient management software, and mobile health (mHealth) apps. The software segment is experiencing rapid growth due to the increasing reliance on digital platforms for healthcare delivery. Telemedicine software and mHealth apps enable virtual consultations, remote monitoring, and patient engagement, making healthcare more accessible and efficient. This segment is expected to continue growing robustly as technology advances and the demand for seamless digital health solutions rises.

The services segment includes the various telehealth services provided to patients, such as virtual consultations, remote monitoring, tele-radiology, tele-ICU, and tele-pharmacy. The services segment is the backbone of the telehealth market, driven by the increasing need for accessible and cost-effective healthcare solutions. Virtual consultations and remote monitoring services have become particularly popular, providing patients with timely medical advice and continuous care without the need for physical visits. The COVID-19 pandemic has accelerated the adoption of these services, highlighting their importance in maintaining healthcare continuity.

- By Type Insights

On the basis of Type, the India telehealth services market is bifurcated into telemedicine, e-consultation, tele-hospitals, and mhealth.

Telemedicine involves the use of digital communication technologies to provide clinical healthcare remotely. The telemedicine segment is a key driver of the telehealth market, offering significant advantages in terms of accessibility and convenience, particularly in rural and underserved areas. The segment is experiencing rapid growth due to increasing internet penetration, rising smartphone usage, and the need for remote healthcare solutions exacerbated by the COVID-19 pandemic.

e-Consultation refers to the online consultation services provided by healthcare professionals, typically through dedicated platforms or apps. The e-Consultation segment is growing robustly as more patients and healthcare providers adopt digital platforms for medical consultations. The convenience of accessing healthcare services from home, combined with the increasing availability of user-friendly e-consultation platforms, is driving this segment. e-Consultations help bridge the gap between patients and healthcare providers, ensuring continuity of care and improving patient outcomes. The segment is expected to continue expanding as digital health platforms become more sophisticated and integrated with other healthcare services.

Tele-Hospitals leverage telehealth technologies to extend the reach of hospital services beyond physical locations. This includes tele-ICU, tele-radiology, tele-stroke, and other specialized telehealth services provided by hospitals. Tele-Hospitals are transforming the way specialized healthcare services are delivered, particularly in remote and rural areas. By utilizing telehealth technologies, hospitals can provide critical care services, remote diagnostics, and expert consultations without the need for patients to travel long distances. The segment is expected to grow significantly as hospitals increasingly adopt telehealth solutions to expand their reach and improve patient care.

mHealth, or mobile health, involves the use of mobile devices and applications to deliver health-related services and information. This includes health tracking apps, fitness applications, remote monitoring tools, and wellness apps. The mHealth segment is one of the fastest-growing areas in the telehealth market, driven by the widespread use of smartphones and mobile internet. mHealth applications provide a wide range of services, from chronic disease management and medication reminders to fitness tracking and mental health support. The increasing adoption of wearable devices and the integration of AI and data analytics in mHealth apps are further enhancing their capabilities.

- By Application Insights

Based on Application, the India telehealth services market is categorized into teleradiology, telepsychiatry, teledermatology, telepathology, telecardiology, teleconsultation, and others.

Teleradiology is a critical component of telehealth services, enabling timely and accurate diagnosis of medical conditions, especially in remote and underserved areas. The segment is driven by the increasing demand for radiological services, the shortage of radiologists in rural areas, and advancements in imaging technology and digital communication.

Telepsychiatry is gaining prominence due to the rising awareness of mental health issues and the increasing need for accessible mental health services. The segment is supported by the growing acceptance of remote consultations for mental health, the stigma reduction associated with seeking psychiatric help, and the convenience of receiving care from home. The COVID-19 pandemic has further accelerated the adoption of telepsychiatry, highlighting its importance in providing continuous mental health support. The segment is expected to see robust growth as mental health awareness and demand for psychiatric services continue to rise.

Teledermatology offers significant advantages in terms of accessibility and convenience, particularly for patients in remote areas who may not have easy access to dermatologists. The segment is driven by the increasing prevalence of skin conditions, the growing demand for specialist consultations, and the ability to provide quick and accurate diagnoses through digital imaging. Teledermatology is expected to grow steadily as more healthcare providers adopt telehealth solutions to enhance dermatological care.

Telepathology is essential for improving diagnostic accuracy and speed, particularly in regions with limited access to specialized pathology services. The segment is driven by advancements in digital pathology, the need for timely and accurate diagnoses, and the integration of AI and machine learning for enhanced image analysis. Telepathology is expected to grow as healthcare facilities seek to improve diagnostic capabilities and patient outcomes through remote pathology services.

Telecardiology is critical for managing chronic cardiovascular conditions and providing timely interventions, especially in remote areas. The segment is driven by the increasing prevalence of heart diseases, the need for continuous cardiac monitoring, and the advancements in wearable devices and remote monitoring technologies. Telecardiology is expected to grow significantly as the demand for cardiac care rises and telehealth solutions become more integrated into routine healthcare practices.

Teleconsultation is the most widely adopted telehealth application, driven by its convenience, cost-effectiveness, and ability to provide timely medical advice. The segment is supported by the increasing adoption of digital health platforms, the growing acceptance of remote consultations, and the need for accessible healthcare services. The COVID-19 pandemic has significantly boosted the adoption of teleconsultation, making it an integral part of the healthcare system. The segment is expected to continue its strong growth trajectory as telehealth becomes more mainstream.

Recent Developments:

- Apollo Telehealth Boosts Critical Care (September 2023): Apollo Telehealth, a leading player, launched Tele-Emergency ICU services across nine NTPC plants. This initiative utilizes telehealth technology to provide remote medical supervision and support during emergencies, enhancing critical care capabilities.

- Reliance Strengthens Digital Healthcare Presence (April 2022): Reliance Retail, a major Indian player, acquired a 60% stake in Netmeds, an online pharmacy platform, for $80 million. This strategic move signals Reliance's intent to expand its presence in the digital healthcare market, with plans to increase its share in Netmeds to 80% by 2024.

Report Scope

Report Attribute |

Details |

Market Size in 2023 |

USD 3.35 Billion |

Projected Market Size in 2032 |

USD 10.47 Billion |

CAGR Growth Rate |

13.5% CAGR |

Base Year |

2023 |

Forecast Years |

2024-2032 |

Key Market Players |

1 mg, Apollo Health, DocsApp, Doctor 24×7, Doctor Insta, HealthifyMe, Lybrate, MediBuddy, Medlife, mfine, NetMeds, Niramai, PharmEasy, Portea Medical, Practo, Tata Health, TeleVital, and Others. |

Key Segment |

By Component, By Type, By Application, By End-User, and By Region |

Regions Covered in India |

North India, South India, East India, West India, and Central India |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Regional Analysis

- South India leads the India telehealth services market, followed closely by North and West India

South India, particularly states like Karnataka and Tamil Nadu, leads the market due to its robust healthcare infrastructure, high literacy rates, and strong government support for digital health initiatives. Cities like Bangalore and Chennai serve as major hubs for healthcare and technology, fostering a favorable environment for telehealth services. South India dominates the telehealth services market with the highest projected CAGR, reflecting its significant contribution to innovation and adoption of telehealth solutions, bolstered by its leadership in IT and digital technologies.

North India, including states such as Delhi, Uttar Pradesh, Punjab, and Haryana, is also a significant market for telehealth services. The region benefits from high levels of internet penetration, advanced healthcare infrastructure, and a large urban population that is increasingly adopting digital health solutions. The presence of numerous hospitals, clinics, and healthcare startups in Delhi NCR drives the growth of telehealth services. North India is expected to see substantial growth, driven by increasing awareness and adoption of digital health technologies, supported by government initiatives to enhance digital healthcare access.

West India, particularly Maharashtra, is another key region for telehealth services. Mumbai, the financial capital of India, has a high concentration of healthcare facilities, technology companies, and startups, driving the adoption of telehealth solutions. Pune is also emerging as a significant hub for digital health. The region is expected to grow significantly, supported by high urbanization, advanced healthcare infrastructure, and increasing digital literacy.

East India, with Kolkata as a major urban center, is an emerging market for telehealth services. Despite challenges such as lower internet penetration and limited healthcare infrastructure, increasing government efforts to improve healthcare access and digital connectivity are driving growth in this region. East India is expected to see steady growth as infrastructure improves and digital health initiatives expand, supported by efforts to bridge the healthcare gap in rural and underserved areas through telehealth services.

Central India, including states like Madhya Pradesh and Chhattisgarh, represents a smaller market for telehealth services compared to other regions. However, it is witnessing gradual growth due to rising urbanization and increasing awareness about digital health solutions. The region has significant potential for growth as local governments and healthcare providers work to improve telehealth infrastructure. Central India is expected to grow as internet penetration increases and telehealth services become more accessible, driven by initiatives to improve healthcare delivery in remote and rural areas.

List of Key Players

The analysis-intensive report provides key insights into companies and organizations operating in the India telehealth services market. The study further makes a relative examination of the organizations highlighting essential business parameters such as geographic presence, business overviews, product offerings, segment-based market share, operational strategies, and SWOT analysis. Recent enterprise developments including novel product launches, joint ventures, partnerships, strategic alliances, mergers & acquisitions, and product development are elaborated upon in the report. The in-depth study thus facilitates a comprehensive analysis of market competition.

Some of the main competitors dominating the India telehealth services market include;

- 1 mg

- Apollo Health

- DocsApp

- Doctor 24×7

- Doctor Insta

- HealthifyMe

- Lybrate

- MediBuddy

- Medlife

- mfine

- NetMeds

- Niramai

- PharmEasy

- Portea Medical

- Practo

- Tata Health

- TeleVital

The India telehealth services market is segmented as follows:

By Component

- Hardware

- Software

- Services

By Type

- Telemedicine

- e-Consultation

- Tele-Hospitals

- mHealth

By Application

- Teleradiology

- Telepsychiatry

- Teledermatology

- Telepathology

- Telecardiology

- Teleconsultation

- Others

By End-User

- Providers

- Patients

- Others

By Region

- North India

- South India

- East India

- West India

- Central India

Industry Major Market Players

- 1 mg

- Apollo Health

- DocsApp

- Doctor 24×7

- Doctor Insta

- HealthifyMe

- Lybrate

- MediBuddy

- Medlife

- mfine

- NetMeds

- Niramai

- PharmEasy

- Portea Medical

- Practo

- Tata Health

- TeleVital

Frequently Asked Questions

Copyright © 2024 - 2025, All Rights Reserved, Facts and Factors