![]()

Search Market Research Report

Auto Insurance Market Size, Share Global Analysis Report, 2024 – 2032

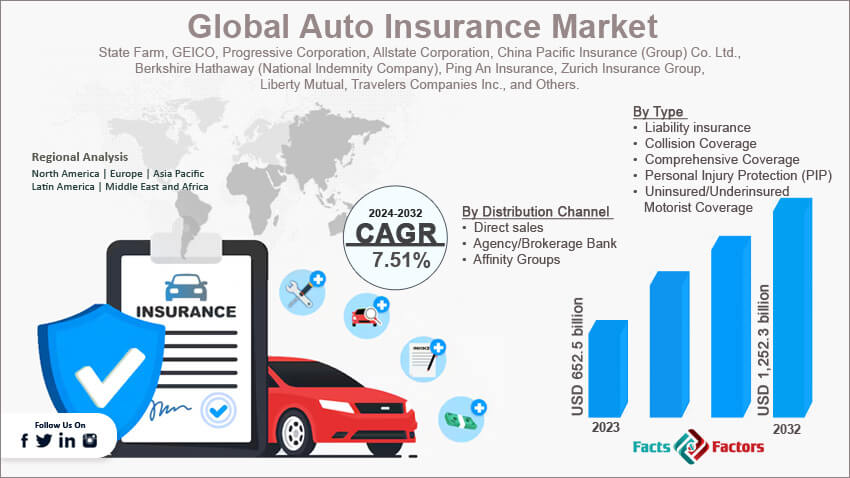

Auto Insurance Market Size, Share, Growth Analysis Report By Type (Liability Insurance, Collision Coverage, Comprehensive Coverage, Personal Injury Protection (PIP), and Uninsured/Underinsured Motorist Coverage), By Distribution Channel (Direct Sales (Online), Agency/Brokerage Bank, and Affinity Groups), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2024 – 2032

Industry Insights

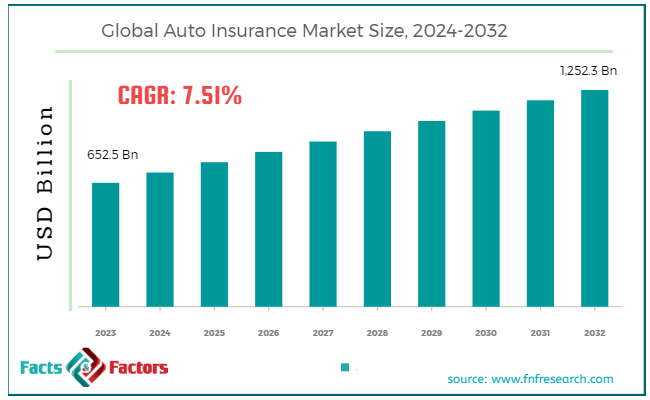

[211+ Pages Report] According to Facts & Factors, the global auto insurance market size in terms of revenue was valued at around USD 652.5 billion in 2023 and is expected to reach a value of USD 1,252.3 billion by 2032, growing at a CAGR of roughly 7.51% from 2024 to 2032. The global auto insurance market is projected to grow at a significant growth rate due to several driving factors.

Market Overview

Market Overview

Auto insurance has become an important part of the automobile industry that protects and covers vehicle owners in the case of an accident, robbery, or other unforeseen occurrence. Insurance is a legal obligation in many countries, and it is intended to reduce the financial risks of the car owners. Auto insurance rules often include many insurance types, each providing certain safeguards.

The fundamental component of vehicle insurance is liability coverage, which covers physical injury and property damage caused by the accident. This coverage is required to satisfy legal requirements and to protect the insured from any litigation.

Moreover, non-collision occurrences such as theft, vandalism, natural disasters, or animal collisions are covered under comprehensive coverage. This coverage is useful for protecting the vehicle from threats other than ordinary accidents. Furthermore, personal injury protection (PIP) or medical payments coverage reimburses the insured driver and passengers for medical expenditures incurred in the event of a collision, regardless of responsibility.

Key Highlights

- The auto insurance market has registered a CAGR of 7.51% during the forecast period.

- In terms of revenue, the global auto insurance market was estimated at roughly USD 652.5 billion in 2023 and is predicted to attain a value of USD 1,252.3 billion by 2032.

- Global auto insurance is projected to grow at a significant rate due to growing vehicle ownership, technological advancements, and a heightened focus on risk mitigation & safety measures.

- Based on type, the liability insurance segment was predicted to hold the maximum market share in the year 2023.

- On the basis of distribution channel, the direct sales segment is projected to swipe the largest market share.

- By region, Asia Pacific was the leading revenue generator in 2023 and is expected to dominate the global market during the forecast period.

Growth Drivers:

- Increasing integration of telematics and advanced technologies is propelling the market growth

The increasing integration of telematics and sophisticated technology to analyze driving behavior and tailor insurance prices is a significant driver in the auto insurance industry. Telematics is the monitoring and collection of data on many elements of driving, such as speed, acceleration, braking, and location. This data is used by insurers to get insights into persons driving performances and allow more accurate risk assessment. Drivers who exhibit better driving behaviors may be eligible for lower insurance rates or other incentives. Telematics not only benefits insurance firms by improving risk prediction, but it also benefits policyholders. Safe drivers can reduce their insurance prices based on real driving performance rather than general demographic criteria. This tailored method coincides with client demands for honest and personalized pricing, establishing a pleasant relationship between insurers and policyholders.

As technology advances and more automobiles are outfitted with connectivity features, the combination of telematics is likely to be a significant driving force shaping the future of the automobile coverage marketplace, promoting a shift toward more customized and data-driven insurance models.

Restraints:

- Economic downturns or significant global events may restrain market growth

The growth of the auto insurance industry may be restrained due to external factors such as economic downturns or global catastrophes. Uncertainty in the economy, recessions, or unexpected catastrophes such as the COVID-19 pandemic can cause changes in consumer spending behavior. People may consider removing unnecessary spending on insurance during financially difficult times. This may result in a lessened interest in comprehensive vehicle insurance coverage. In addition, economic volatility makes it difficult for insurance providers to forecast and adjust to changes in customer demand and financial objectives. This ultimately has an impact on overall market stability.

Furthermore, stringent regulatory processes and varied criminal requirements in different countries might slow down the automotive insurance business. Compliance with various and shifting rules necessitates insurers navigating complicated felony landscapes, which adds administrative overhead and may impact their ability to deliver uniform and standardized products. Plus, adhering to multiple legal frameworks necessitates a high level of adaptability and flexibility from insurers. Such complexity may also impede operational efficiency and innovation in some areas.

Opportunities:

- Ongoing development of innovative technologies to provide growth opportunities

The car insurance sector is undergoing a significant transition as a result of the extensive integration of artificial intelligence (AI) and data analytics. This technological explosion with AI creates huge potential for risk assessment, price optimization, claims processing, and fraud detection. Looking at the stats 6.7 million reported automotive incidents, 38,824 fatalities, and 2.3 million injuries in the United States in 2020. Integration of Artificial intelligence (AI) and machine learning algorithms in the industry can be used to evaluate large amounts of data that can help in accident prevention and mitigation.

Furthermore, usage-based insurance (UBI) is gaining traction, allowing insurers to modify prices based on actual driving behavior, increasing consumer loyalty and competitiveness. These developments will not only increase operational efficiency but also herald a new age of auto insurance innovation and data-driven excellence.

Challenges:

- Increasing complexity and frequency of cybersecurity threats to challenge market growth

The rising complexity and frequency of cybersecurity attacks pose a substantial issue in the vehicle insurance sector. With the integration of telematics, linked automobiles, and online platforms, the number of sensitive data gathered and held by insurers has increased substantially. With the increasing sale of online insurance, the sector has become more vulnerable to cyberattacks such as data breaches and ransomware assaults.

Furthermore, the altering automotive landscape coupled with the growth of self-sufficient and connected autos poses a challenge for existing insurance models. The move to autonomous use presents issues about legal liability and threat assessment, as accidents might include not only human errors but also technological failures or software program flaws. Insurers must adjust their underwriting models and risk assessment procedures to account for emerging technologies, ensuring that recommendations remain appropriate, true, and economically practical. Navigating the intricacies of insuring vehicles with advanced technology necessitates a proactive and progressive approach to keep up with the expanding automotive landscape and the associated risks.

Auto Insurance Market: Segmentation Analysis

The global auto insurance market is segmented based on type, distribution channel, and region.

By Type Insights

Based on type, the global auto insurance market segments are liability insurance, collision coverage, comprehensive coverage, personal injury protection (pip), and uninsured/underinsured motorist coverage. In 2023, the liability insurance category has established dominance in the worldwide auto insurance industry. This is mainly due to its critical function in providing basic coverage. Liability insurance provides financial protection for policyholders if they are at fault in an accident, covering damages and bodily injuries inflicted on others. Plus, its extensive usage is motivated by legal obligations and the fundamental need to protect against potential liabilities.

By Distribution Channel Insights

In terms of distribution channel, the global auto insurance market is categorized as direct sales (online), agency/brokerage banks, and affinity groups. In 2023, direct sales (online) have emerged as the largest segment in the global auto insurance industry. The large share of the segment is attributed to the rising digitization of insurance services and shifting customer preferences. With the online channels, customers can quickly compare plans, request rates, and purchase vehicle insurance directly from insurers. Furthermore, the need for simplicity, openness, and instant access to information is driving this move toward direct Internet sales.

Recent Developments:

- In 2022, Allstate launched the Milewise Program, introducing distance-based insurance with customizable choices targeted to both infrequent and high-mileage drivers. Concurrently, Metromile released its Per-Trip Insurance Product, which caters to infrequent drivers and car-sharing users by providing short-term coverage for individual automobile rides, exemplifying an industry trend toward more tailored and usage-specific insurance solutions.

- In 2021, by acquiring Aviva's Italian business Allianz strengthened its position in Europe's fourth-largest vehicle insurance market, expanding its regional reach. Simultaneously, Lemonade acquired Metromile and expanded its novel pay-per-mile insurance model into California and other U.S. states, signaling a deliberate effort to widen its impact on the American insurance scene.

Report Scope

Report Attribute |

Details |

Market Size in 2023 |

USD 652.5 Billion |

Projected Market Size in 2032 |

USD 1,252.3 Billion |

CAGR Growth Rate |

7.51% CAGR |

Base Year |

2023 |

Forecast Years |

2024-2032 |

Key Market Players |

State Farm, GEICO, Progressive Corporation, Allstate Corporation, China Pacific Insurance (Group) Co. Ltd., Berkshire Hathaway (National Indemnity Company), Ping An Insurance, Zurich Insurance Group, Liberty Mutual, Travelers Companies Inc., and Others. |

Key Segment |

By Type, By Distribution Channel, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Auto Insurance Market: Regional Analysis

- Asia Pacific to lead the market during the forecast period

The Asia Pacific region is expected to dominate the auto insurance market during the forecast period, owing several major factors that contribute to the area's dynamic expansion in the automotive and insurance sectors. Rapid urbanization, a growing middle class, and rising disposable income have resulted in a major increase in automobile ownership in nations such as China and India. As legal requirements and knowledge of the significance of insurance coverage continue to expand, the increase in the number of vehicles on the road generates a sizable market for auto insurance.

Furthermore, technological improvements, notably the increasing use of smartphones and digital platforms, have aided the expansion of insurance distribution channels. Consumers in the Asia Pacific area have embraced digitization, with an increased reliance on online channels.

The simplicity and accessibility of digital platforms contribute to the expansion of the region's vehicle insurance industry, allowing insurers to reach a bigger consumer base and offer new products and services. The Asia Pacific region's leadership in the vehicle insurance industry is projected to continue as the automotive and insurance landscapes shift. The area plays a crucial role in defining the future of the car insurance sector due to a growing vehicle market, greater awareness of insurance needs, and rapid use of digital technology.

APAC was estimated to hold around 44% of global automobile sales in 2022. This figure is expected to increase as the middle-class population in the region is predicted to reach 5.5 billion by 2032. With the growth in the middle-class population and increase in disposable income, there will be a bulging demand for automobile ownership which in turn will support the auto insurance market. Many APAC developed and emerging nations like India, China, and Malaysia, have made compulsion for vehicle insurance, which increases market penetration even more.

Some of the key players such as Ping An Insurance (China), Tokio Marine Holdings (Japan), Samsung Fire & Marine Insurance (South Korea), Bajaj Allianz General Insurance (India), and other big firms with considerable market share and resources to engage in AI and data analytics are among the leading players.

Auto Insurance Market: Competitive Landscape

The analysis-intensive report provides key insights into companies and organizations operating in the global auto insurance market. The study further makes a relative examination of the organizations highlighting essential business parameters such as geographic presence, business overviews, product offerings, segment-based market share, operational strategies, and SWOT analysis. Recent enterprise developments including novel product launches, joint ventures, partnerships, strategic alliances, mergers & acquisitions, and product development are elaborated upon in the report. The in-depth study thus facilitates a comprehensive analysis of market competition.

Some of the main competitors dominating the global auto insurance market include;

- State Farm

- GEICO

- Progressive Corporation

- Allstate Corporation

- China Pacific Insurance (Group) Co., Ltd.

- Berkshire Hathaway (National Indemnity Company)

- Ping An Insurance

- Zurich Insurance Group

- Liberty Mutual

- Travelers Companies Inc.

The global auto insurance market is segmented as follows:

By Type Segment Analysis

- Liability insurance

- Collision Coverage

- Comprehensive Coverage

- Personal Injury Protection (PIP)

- Uninsured/Underinsured Motorist Coverage

By Distribution Channel Segment Analysis

- Direct sales

- Agency/Brokerage Bank

- Affinity Groups

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- State Farm

- GEICO

- Progressive Corporation

- Allstate Corporation

- China Pacific Insurance (Group) Co., Ltd.

- Berkshire Hathaway (National Indemnity Company)

- Ping An Insurance

- Zurich Insurance Group

- Liberty Mutual

- Travelers Companies Inc.

Copyright © 2024 - 2025, All Rights Reserved, Facts and Factors