![]()

Search Market Research Report

Offshore Wind Energy Market Size, Share Global Analysis Report, 2024 – 2032

Offshore Wind Energy Market Size, Share, Growth Analysis Report By Component (Turbine, Support Structure, Electrical Infrastructure, and Others), By Location (Deep Water, Shallow Water, and Transitional Water), By Depth (0 to = 30 m, 30 to = 50 m, 50 m), and By Region - Global and Regional Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2024 – 2032

Industry Insights

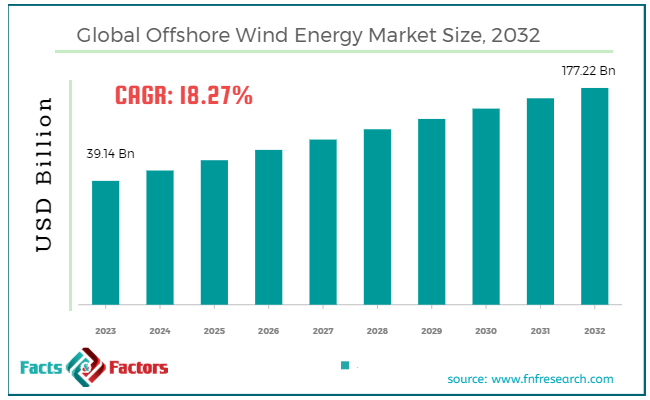

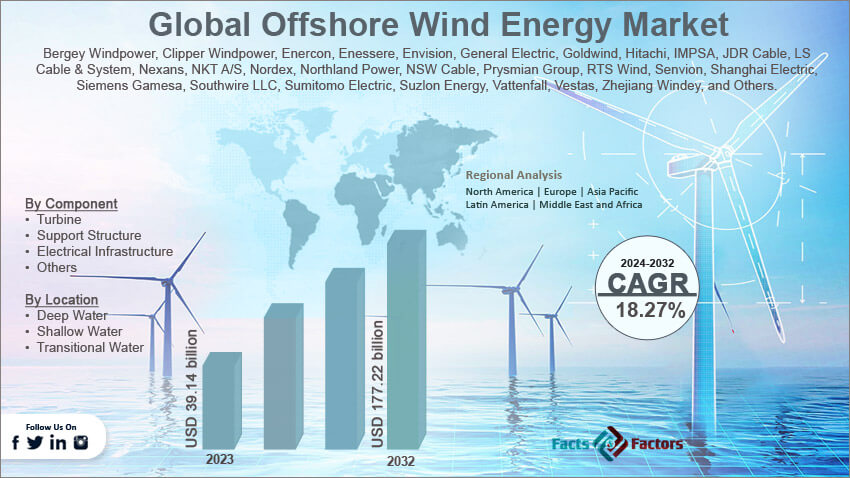

[221+ Pages Report] According to Facts & Factors, the global offshore wind energy market size in terms of revenue was valued at around USD 39.14 billion in 2023 and is expected to reach a value of USD 177.22 billion by 2032, growing at a CAGR of roughly 18.27% from 2024 to 2032. The global offshore wind energy market is projected to grow at a significant growth rate due to several driving factors.

Market Overview

Market Overview

Offshore wind energy is a form of power generation where wind turbines are installed in large bodies of water, usually oceans or large lakes, to harness the kinetic energy of wind and convert it into electricity. These installations are typically placed far from shore to capitalize on the more consistent and stronger winds found at sea, compared to those on land. Offshore wind farms have the advantage of reduced visual and noise impacts on communities and often encounter fewer objections than onshore installations.

The technology behind offshore wind includes larger turbines and foundations anchored to the ocean floor, which can be significantly more complex and expensive than those used on land. However, the higher wind speeds accessible offshore make these turbines more efficient, producing more energy per unit than their onshore counterparts.

As a crucial part of the transition to renewable energy, offshore wind helps reduce carbon emissions and reliance on fossil fuels, contributing to energy security and environmental sustainability. The field is advancing rapidly, with innovations in turbine technology and floating platforms that allow for deployment in deeper waters, expanding the potential for future offshore wind development.

Key Highlights

- The offshore wind energy market has registered a CAGR of 18.27% during the forecast period.

- In terms of revenue, the global offshore wind energy market was estimated at roughly USD 39.14 billion in 2023 and is predicted to attain a value of USD 177.22 billion by 2032.

- The growth of the offshore wind energy market is being propelled by rising demand for clean energy, considerable investments and technological innovations.

- Based on the component, the electrical infrastructure segment is growing at a high rate and is projected to dominate the global market.

- By region, the Europe is projected to dominate the global market due to shallow water and government financing.

Growth Drivers:

- Increasing Demand for Renewable Energy: Concerns about climate change and depleting fossil fuel reserves are driving a global push for clean energy sources. Offshore wind offers a reliable and sustainable alternative, making it attractive to governments and power companies to reduce carbon emissions grow.

- Technological Advancements: The development of larger, more powerful wind turbines and improved foundation designs allows for installations in deeper waters with stronger winds, increasing energy generation potential. Additionally, advancements in floating wind turbine technology open up possibilities for locations previously inaccessible.

- Government Incentives and Support: Many countries provide subsidies and tax incentives for renewable energy projects, including offshore wind, which reduce the financial burden on developers and promote rapid growth.

- Decreasing Costs: Technological advancements and economies of scale are leading to a gradual decrease in the cost of developing and operating offshore wind farms. This is making offshore wind a more cost-competitive source of electricity.

Restraints:

- High Upfront Costs: Despite cost reductions, offshore wind projects still require significant upfront investment compared to some traditional energy sources. This can be a barrier for some developers and investors.

- Environmental and Maritime Impact: Potential impacts on marine life during construction and operation of offshore wind farms raise concerns. Mitigation strategies and careful environmental impact assessments are crucial for responsible development.

- Transmission Infrastructure: Connecting offshore wind farms to the electricity grid requires significant investment in subsea cables. Building and maintaining this infrastructure can be complex and expensive.

- Siting Challenges: Finding suitable locations for offshore wind farms requires balancing factors such as wind resource potential, environmental impact, and proximity to existing transmission infrastructure. Additionally, visual and social impacts on coastal communities need to be considered.

Opportunities:

- Floating Wind Technology: This emerging technology allows for wind farm development in deeper waters further from shore, unlocking vast untapped wind resources.

- Integration with Other Renewable Technologies: Offshore wind energy can be combined with other forms of energy production, like solar or tidal, to create hybrid systems that offer more consistent power output.

- Offshore Wind Farm Optimization: Advances in data analytics and machine learning can optimize wind farm operations, leading to increased efficiency and energy production.

- Wind and Energy Storage Integration: Integration with energy storage solutions can help address the variability of wind power, making it a more reliable source of baseload electricity.

Challenges:

- Public Perception: Some communities may have concerns about the visual impact of offshore wind farms or potential impacts on tourism and fishing activities. Effective public engagement and communication strategies are essential to address these concerns.

- Supply Chain Constraints: The rapid growth of the offshore wind industry can lead to challenges in the supply chain for specialized components and vessels needed for construction.

- Geopolitical Issues: Tensions between countries can create complications in developing offshore wind projects in shared maritime areas.

- Decommissioning Costs: Planning and funding for the decommissioning of offshore wind farms at the end of their lifespan needs to be factored into project development.

Offshore Wind Energy Market: Segmentation Analysis

The global offshore wind energy market is segmented based on component, location, depth, and region.

By Component Insights

Based on Component, the global offshore wind energy market is divided into turbine, support structure, electrical infrastructure, and others. The turbine is the most critical component, converting wind energy into electrical energy. It comprises the rotor (blades and hub), nacelle (housing for generating components), and tower. Continuous advancements in turbine technology, such as larger blade designs and higher capacity turbines, drive the market. The focus on reducing the levelized cost of energy (LCOE) motivates innovations like enhanced aerodynamic efficiency and reliability in harsh marine environments??.

Support structures, such as monopiles, jacket foundations, and floating platforms, anchor the turbines to the seabed or float them on the surface. They must withstand marine conditions and support the weight and dynamic loads of the turbines. The choice of structure depends on water depth, seabed condition, and environmental impact considerations. Innovations in design to accommodate deeper waters and reduce costs are key market drivers??.

Electrical Infrastructure segment includes all electrical components necessary for collecting and transmitting the electricity generated by turbines back to shore. Key elements are underwater cables, substations, and transformers. Developments aim to improve the efficiency and reliability of power transmission systems, reduce energy loss, and ensure compatibility with existing grid infrastructure. The expansion of offshore wind installations increases demand for robust and efficient electrical infrastructure?.

By Location Insights

On the basis of Location, the global offshore wind energy market is bifurcated into deep water, shallow water, and transitional water. Deep water locations are defined as areas where the water depth exceeds 60 meters. These locations typically require floating wind turbines because traditional fixed-bottom structures are not feasible.

Floating turbines represent a rapidly growing segment due to their ability to tap wind resources in deep offshore environments previously inaccessible. This segment faces challenges such as higher costs and more complex maintenance, but advances in technology are gradually overcoming these barriers??.

Shallow water locations are those where the depth is less than 30 meters. Most existing offshore wind farms are located in shallow waters using fixed-bottom structures like monopiles and jacket foundations. This is the most established segment with proven technology and lower installation and maintenance costs compared to deeper water projects. The market is driven by easier access and lower technical complexity, making these projects more cost-effective and quicker to deploy??.

Transitional water locations are characterized by depths ranging from 30 to 60 meters. These areas typically use fixed foundations but may start incorporating floating structures as the technology matures. Transitional waters offer potential for expansion as they can utilize both traditional and innovative technologies. Challenges here include balancing cost and technical feasibility, especially as depths approach the upper limit of fixed-bottom capabilities.

Recent Developments:

- In January 2023, The Xience Sierra drug-eluting stent, which is intended to offer greater flexibility and deliverability than earlier models, was introduced by Abbott Laboratories in January 2023.

- In February 2023, The FDA approved Medtronic plc's Onyx Frontier drug-eluting stent in February 2023. The stent comprises a delivery mechanism intended to improve the stent's acute performance and deliverability.

Report Scope

Report Attribute |

Details |

Market Size in 2023 |

USD 39.14 Billion |

Projected Market Size in 2032 |

USD 177.22 Billion |

CAGR Growth Rate |

18.27% CAGR |

Base Year |

2023 |

Forecast Years |

2024-2032 |

Key Market Players |

Bergey Windpower, Clipper Windpower, Enercon, Enessere, Envision, General Electric, Goldwind, Hitachi, IMPSA, JDR Cable, LS Cable & System, Nexans, NKT A/S, Nordex, Northland Power, NSW Cable, Prysmian Group, RTS Wind, Senvion, Shanghai Electric, Siemens Gamesa, Southwire LLC, Sumitomo Electric, Suzlon Energy, Vattenfall, Vestas, Zhejiang Windey, and Others. |

Key Segment |

By Component, By Location, By Depth, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Offshore Wind Energy Market: Regional Analysis

- Europe currently dominates the global offshore wind energy market

Europe is the leader in offshore wind energy, with a well-established infrastructure and the highest number of installed offshore wind farms. Countries like the United Kingdom, Germany, and Denmark are pioneers, hosting some of the world's largest offshore wind projects. The European market benefits from strong governmental support, robust funding mechanisms, and advanced technology. The North Sea is particularly suited for offshore wind developments due to its favorable wind conditions and shallow waters.

Asia-Pacific region is experiencing the fastest growth in offshore wind capacity, led by countries such as China, South Korea, and Taiwan. China, in particular, has rapidly scaled up its installations, aiming to lead in renewable energy production. Asia-Pacific benefits from governmental ambitions to decrease reliance on fossil fuels, significant coastlines, and increasing local expertise in offshore wind installations.

North America has a relatively untapped offshore wind market, with significant potential along the East Coast of the U.S. States like Massachusetts, New York, and New Jersey are beginning to invest heavily in offshore wind projects. The market is supported by state-level renewable energy targets and federal backing. However, it is still in the early stages of development compared to Europe and Asia.

Rest of the World, including Latin America and parts of Africa, are in the early stages of exploring offshore wind energy. These areas have vast untapped potential due to extensive coastlines and growing energy needs. The growth in these regions is hindered by a lack of regulatory frameworks and infrastructure but holds a long-term potential for development. The growth rate is less defined due to the nascent stage of offshore wind projects but is expected to increase as global efforts to combat climate change intensify.

Offshore Wind Energy Market: Competitive Landscape

Some of the main competitors dominating the global offshore wind energy market include;

- Bergey Windpower

- Clipper Windpower

- Enercon

- Enessere

- Envision

- General Electric

- Goldwind

- Hitachi

- IMPSA

- JDR Cable

- LS Cable & System

- Nexans

- NKT A/S

- Nordex

- Northland Power

- NSW Cable

- Prysmian Group

- RTS Wind

- Senvion

- Shanghai Electric

- Siemens Gamesa

- Southwire LLC

- Sumitomo Electric

- Suzlon Energy

- Vattenfall

- Vestas

- Zhejiang Windey

The global offshore wind energy market is segmented as follows:

By Component Segment Analysis

- Turbine

- Support Structure

- Electrical Infrastructure

- Others

By Location Segment Analysis

- Deep Water

- Shallow Water

- Transitional Water

By Depth Segment Analysis

- 0 to ≤ 30 m

- 30 to ≤ 50 m

- 50 m

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Bergey Windpower

- Clipper Windpower

- Enercon

- Enessere

- Envision

- General Electric

- Goldwind

- Hitachi

- IMPSA

- JDR Cable

- LS Cable & System

- Nexans

- NKT A/S

- Nordex

- Northland Power

- NSW Cable

- Prysmian Group

- RTS Wind

- Senvion

- Shanghai Electric

- Siemens Gamesa

- Southwire LLC

- Sumitomo Electric

- Suzlon Energy

- Vattenfall

- Vestas

- Zhejiang Windey

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors