![]()

Search Market Research Report

Aerospace Forging Market Size, Share Global Analysis Report, 2024 – 2032

Aerospace Forging Market Size, Share, Growth Analysis Report By Material Type (Aluminum Alloys, Titanium Alloys, Steel Alloys), By Application (Commercial Aerospace, Military Aerospace, Space Exploration), By End Use (Airframe, Components, Engine Components, Landing Gear), And By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2024 – 2032

Industry Insights

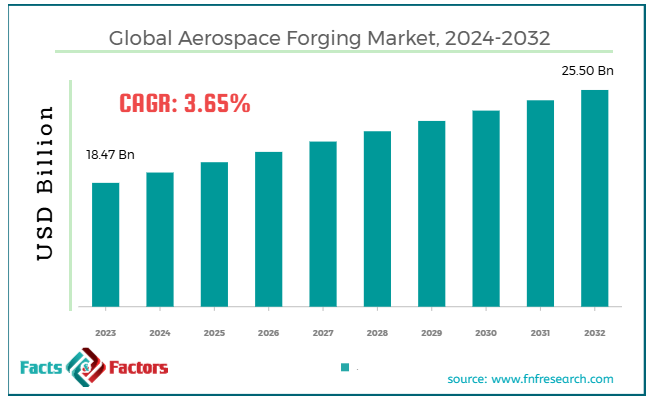

[223+ Pages Report] According to Facts & Factors, the global aerospace forging market size was worth around USD 18.47 billion in 2023 and is predicted to grow to around USD 25.50 billion by 2032, with a compound annual growth rate (CAGR) of roughly 3.65% between 2024 and 2032.

Market Overview

Market Overview

Aerospace forging is a manufacturing practice that helps produce high-performing and strong metal components for aerospace. It comprises shaping metals via regulated deformation, usually with high-pressure devices and machines like presses and hammers, while the metal is heated. The process enhances the durability, strength, and reliability of the materials, thus increasing their suitability for vital aerospace uses. The aerospace forging market is witnessing substantial growth owing to the rising demand for improved technologies and high-performing parts. The key drivers of the market are the rising aircraft production and air traffic and the growing number of technological improvements in aerospace.

With the rising global air traffic and increasing number of passengers, the demand for private and commercial aircraft is also increasing. This ultimately increases the demand for vital parts that need aerospace forging owing to their reliability and superior strength. The aerospace sector also witnesses continuous advancements and innovations like developing highly efficient materials, engines, and parts that demand complex forged components.

However, a few restraining factors negatively impacting the aerospace forging market growth are significant production costs and strict regulatory standards. Aerospace forging comprises complex practices that need enhanced machinery and superior-quality materials, increasing the cost of production processes. This eventually increases the price of aerospace parts, which prevents startups and small manufacturers from purchasing them.

Furthermore, aerospace components should essentially meet the safety regulations and strict quality needs for manufacturers to maintain ideal standards in forging practices. Compliance with such regulations may increase cost and complexity, thus restricting the industry's growth.

Still, the market is opportune to opportunities like the rising trend of sustainability. The aerospace industry is actively emphasizing sustainability practices like increasing fuel efficiency and decreasing carbon footprints, thus impacting market progress.

Key Insights:

- As per the analysis shared by our research analyst, the global aerospace forging market is estimated to grow annually at a CAGR of around 3.65% over the forecast period (2024-2032)

- In terms of revenue, the global aerospace forging market size was valued at around USD 18.47 billion in 2023 and is projected to reach USD 25.50 billion by 2032.

- The aerospace forging market is projected to grow significantly due to the growing number of technological improvements in aerospace, increasing air traffic, and expanding demand for lightweight components.

- Based on material type, the aluminum alloys segment is the dominating segment among others, while the titanium alloys segment is projected to witness sizeable revenue over the forecast period.

- Based on application, the commercial aerospace segment is expected to lead the market, while the military aerospace segment is expected to register considerable growth.

- Based on end use, the airframe components segment is expected to lead the market as compared to the engine components segment.

- Based on region, North America is projected to dominate the global market during the estimated period, followed by Europe.

Growth Drivers

- Steady number of technological innovations in aerospace to boost the market growth

Technological advancements, mainly in engine performance, design efficiency, and material science, are considerably impacting the demand for enhanced forged components. Advanced engines, for example, are specially designed to function at extreme pressures and temperatures, needing advanced materials like nickel and titanium alloys that are manufactured via forging. This trend is also marked in manufacturing and designing lightweight and highly efficient aircraft.

Among other advancements, the Rolls-Royce UltraFan engine is projected to be in service in the late 2020s. This is an example of a high-performing engine needing enhanced forged parts. The UltraFan will provide greater fuel efficiency (25%) than the former models, focusing on the need for high-strength and lightweight forged materials in engine production.

Furthermore, Boeing has significantly invested in the production of sustainable aircraft that need enhanced forging practices for their highly efficient and lighter parts. For instance, the 777X is projected to be extra fuel-efficient and release fewer emissions that comply with the global ecological goals.

- Defense and military expansion are among the major market propellants

Another leading driver of the global aerospace forging market is the growth and progress of the defense and military industry. The global investment in defense is rising substantially, resulting in the production of a number of military aerospace systems like drones, helicopters, fighter jets, and several space exploration vehicles. Forged parts are essential for the making of military aircraft, making sure they can efficiently tolerate high operational environments.

F-35 fighter jet, an advanced military aircraft by Lockheed Martin, has adopted forged parts in vital systems like the airframe and the engine. The demand for these parts has been expanding owing to the current contracts between the United States and the allied nations, thus driving the market.

Moreover, several private space firms and NASA are increasing the number of spacecraft productions. For instance, the SpaceX Starship needs improved forging techniques for its engine parts like SuperDraco engines. These parts need superior-strength alloys to tolerate high space travel conditions.

Restraints

- Disturbances in the supply chain hamper the market progress

The aerospace forging industry is highly dependent on the supply chain for components, vital parts, and raw materials. Disturbances to this supply chain due to factors such as natural disasters, pandemics, geopolitical stresses, or trade restrictions may significantly impact the cost of materials and availability for aerospace forging. These instabilities may delay production schedules and lead to increased prices for forgings.

As per IATA, in 2022, the global freight volumes were reported less owing to disturbances in air cargo and shipping networks, leading to delivery delays of vital materials to forging services.

Furthermore, the Ukraine war in 2022 resulted in key disturbances in the raw materials supply. They comprise nickel, aluminum, and more that are essential for aerospace forgings. The permissions on Russia, a leading supplier of certain materials, resulted in material scarcity and price hikes, impacting the availability and cost of the forged components.

Opportunities

- Development of hybrid forging and additive manufacturing to notably affect the market growth

The incorporation of additive manufacturing with conventional forging techniques, often known as hybrid forging, is an important opportunity for the aerospace forging industry. Hybrid forging combines the benefits of additive manufacturing with the durability and strength of forged components. This approach may substantially decrease production lead times, material wastage, and costs while enhancing the performance and design flexibility of aerospace components.

Hybrid manufacturing offers benefits like decreasing material wastage by restrictively adding materials where required and improving the mechanical characteristics of the components. Research has disclosed that hybrid forging methods may notably enhance the strength-to-weight ratio of aerospace components, which is vital for the aerospace industry.

In 2023, GE Aviation declared it would incorporate hybrid additive manufacturing in its turbine engine production. The company is blending 3D printing with conventional forging methods to develop highly fuel-efficient and lighter components. This hybrid practice enables complex designs that will be impossible to produce using conventional forging.

Challenges

- Cost pressure on labor and raw materials is a barrier to market growth

Increasing costs of labor, raw materials, and energy majorly pressurize the profitability of aerospace forging parts. The aerospace sector needs high-performing materials like advanced titanium and alloys, whose costs are unstable owing to demand and supply dynamics. In addition, aerospace forging manufacturers are witnessing high labor costs, mainly because the demand for skilled labor is growing in the manufacturing sector.

In 2023, Airbus witnessed increasing costs owing to scarcity of labor and material price hikes. Subsequently, the company reported delays in meeting its targets, thus underlining the direct impact of these pressures on manufacturing, comprising forging.

Report Scope

Report Attribute |

Details |

Market Size in 2023 |

USD 18.47 Billion |

Projected Market Size in 2032 |

USD 25.50 Billion |

CAGR Growth Rate |

3.65% CAGR |

Base Year |

2023 |

Forecast Years |

2024-2032 |

Key Market Players |

Arconic Inc., VSMPO-AVISMA Corporation, Doncasters Group Ltd., Forgital Group, Precision Castparts Corp., Magellan Aerospace Corporation, Aero Metals Inc., Park Aerospace Corp., STUBBORN METAL PRODUCTS INC., LISI Aerospace, Allegheny Technologies Incorporated (ATI), Samcor Metal Products Inc., Schaal Engineering GmbH, Kobe Steel Ltd., Boeing Distribution Services Inc., and Others. |

Key Segment |

By Material Type, By Application, By End Use, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Segmentation Analysis

The global aerospace forging market is segmented based on material type, application, end-use, and region.

Based on material type, the global aerospace forging industry is divided into aluminum alloys, titanium alloys, and steel alloys. The aluminum alloys segment held a notable share of the market owing to its lightweight nature and ideal strength-to-weight ratio. The lightweight nature of this material holds significance in various aerospace applications. They majorly reduce overall aircraft weight, resulting in enhanced fuel efficiency, low operational costs, and long range. This ultimately increases the suitability of aluminum in military and commercial applications. The said material also offers a favorable strength-to-weight, thus offering enough strength while being lightweight than most other metals. This is important for multiple aerospace parts like fuselages, engine parts, and wings, which should tolerate high stress and extreme conditions.

Based on application, the global aerospace forging industry is segmented as commercial aerospace, military aerospace, and space exploration. In 2023, the commercial segment marked a considerable share of the market, while the military aerospace registered as the fastest growing. The reasons for the growth of the commercial aerospace segment include technological improvements in aircraft designs and reliability and safety needs.

Improvements in aircraft design, mainly in fuel efficiency and material science, have increased dependency on high-strength forged parts. Manufacturers are emphasizing decreasing weight and improving the durability of vital components like engines and airframes, which use forged materials. Moreover, in aerospace, reliability and safety play a vital role in meeting stringent protocols. Forging practices produce parts with high mechanical characteristics like reliability, high strength, and resistance to exhaustion, which is important for applications where failures are no option.

Based on end use, the global market is segmented into airframe components, engine components, and landing gear. The airframe components segment is projected to hold a maximum share of the market owing to its growing demand for durability and structural integrity. These components must essentially tolerate extreme environmental conditions and high stresses during travel, thus increasing the significance of forged materials. Forging practices enhance the mechanical properties of materials, leading to components with high reliability, strength, and exhaustion-resistance needed for airframes.

Regional Analysis

- North America to hold substantial growth over the forecast period

North America registers a considerable share of the aerospace forging market, followed by Europe. Among other nations, the United States is home to the leading number of aerospace companies like Lockheed Martin, Raytheon, Boeing, and Northrop Grumman, which fuel the demand for quality forged components in military and commercial applications. North America also registers a notable share in defense and space exploration, which drives the demand for forged components.

Moreover, the region has a well-developed infrastructure for enhanced forging and manufacturing technologies, comprising innovation in material science and high-precision forging equipment. The operating companies are the leading adopters of artificial intelligence, automation, and additive manufacturing in forging.

Europe is the second-leading region in the global market owing to the presence of multiple aerospace manufacturers and strong defense and aerospace investment. Europe is also home to several leading manufacturers like Rolls-Royce, Airbus, and Safran, which significantly impact the demand for forged components in the defense and aerospace industries.

Airbus produces nearly more than 600 aircraft yearly, marking its name among the largest manufacturers on a global scale. The region also holds heavy investment and defense spending, mainly in France, Germany, and the United Kingdom. This ultimately increases the need for aerospace forgings for military uses like helicopters and fighter jets.

European defense spending was predicted to exceed USD 300 million, thus propelling the demand for high-performing forgings.

Competitive Analysis

The global aerospace forging industry is led by players like:

- Arconic Inc.

- VSMPO-AVISMA Corporation

- Doncasters Group Ltd.

- Forgital Group

- Precision Castparts Corp.

- Magellan Aerospace Corporation

- Aero Metals Inc.

- Park Aerospace Corp.

- STUBBORN METAL PRODUCTS INC.

- LISI Aerospace

- Allegheny Technologies Incorporated (ATI)

- Samcor Metal Products Inc.

- Schaal Engineering GmbH

- Kobe Steel Ltd.

- Boeing Distribution Services Inc.

Key Market Trends

- Growing use of advanced alloys:

At present, the use of advanced materials like nickel-based alloys and titanium alloys has surged significantly. These materials offer the optimum level of strength-to-ratio, high performance, and corrosion resistance. This increases their suitability for numerous military and commercial applications.

- Rising use of AI and automation in forging:

Currently, aerospace forging manufacturers are actively implementing artificial intelligence and automation technologies to enhance efficiency, precision, and significantly decrease human errors during production. These technologies help improve quality control, simplify production lines, and reduce operational costs.

The global aerospace forging market is segmented as follows:

By Material Type Segment Analysis

- Aluminum Alloys

- Titanium Alloys

- Steel Alloys

By Application Segment Analysis

- Commercial Aerospace

- Military Aerospace

- Space Exploration

By End Use Segment Analysis

- Airframe Components

- Engine Components

- Landing Gear

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

- Arconic Inc.

- VSMPO-AVISMA Corporation

- Doncasters Group Ltd.

- Forgital Group

- Precision Castparts Corp.

- Magellan Aerospace Corporation

- Aero Metals Inc.

- Park Aerospace Corp.

- STUBBORN METAL PRODUCTS INC.

- LISI Aerospace

- Allegheny Technologies Incorporated (ATI)

- Samcor Metal Products Inc.

- Schaal Engineering GmbH

- Kobe Steel Ltd.

- Boeing Distribution Services Inc.

Copyright © 2024 - 2025, All Rights Reserved, Facts and Factors