![]()

Search Market Research Report

Climate Tech Market Size, Share Global Analysis Report, 2024 – 2032

Climate Tech Market Size, Share, Growth Analysis Report By Components (Services And Climate Tech Solutions), By Technologies (Blockchain, Security, Cloud Computing, Digital Twins, AI & Analytics, IoT, And Others), By Applications (Sustainable Mining & Exploration, Weather Monitoring And Forecasting, Forest Monitoring, Crop Monitoring, Water Purification, Carbon Footprint Management, And Green Building), And By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2024 – 2032

Industry Insights

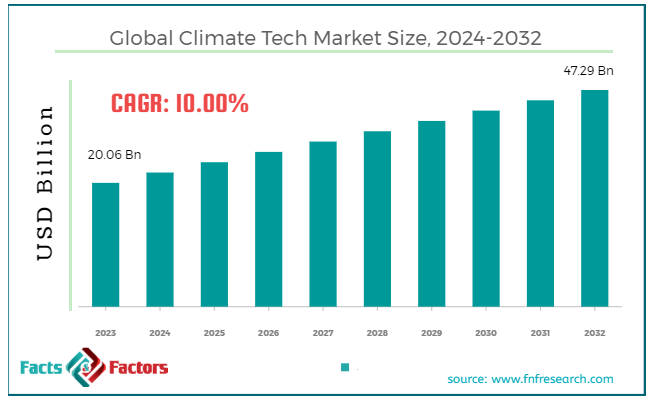

[216+ Pages Report] According to Facts & Factors, the global climate tech market size was valued at USD 20.06 billion in 2023 and is predicted to surpass USD 47.29 billion by the end of 2032. The climate tech industry is expected to grow by a CAGR of 10.00% between 2024 and 2032.

Market Overview

Market Overview

Climate tech refers to climate technology, which includes a broad spectrum of innovations, solutions, and technologies that help eliminate or lower the negative impact on climate. These technologies promote renewable energy sources, improve energy efficiency and lower greenhouse gas emissions. Climate tech helps mitigate climate change, thereby helping slow global warming.

Moreover, climate also helps in preparing for the consequences of climate change. Climate tech also helps promote sustainable development all across the globe by lowering dependence on traditional fossil fuels and offering energy independence.

Key Insights

- As per the analysis shared by our research analyst, the global climate tech market size is estimated to grow annually at a CAGR of around 10.00% over the forecast period (2024-2032).

- In terms of revenue, the global climate tech market size was valued at around USD 20.06 billion in 2023 and is projected to reach USD 47.29 billion by 2032.

- Regulatory policies are driving the growth of the global climate tech market.

- Based on the components, the climate tech solutions segment is growing at a high rate and is projected to dominate the global market.

- Based on the technologies, the blockchain segment is projected to swipe the largest market share.

- Based on applications, the carbon footprint management segment is expected to dominate the global market.

- Based on region, North America is expected to dominate the global market during the forecast period.

Growth Drivers

- Regulatory policies are driving the growth of the global market.

Regulatory policies all across the globe are issuing mandates to curb greenhouse gas emissions. They are coming up with regulations like renewable energy mandates, subsidies for clean technology, and carbon pricing, which in turn are likely to positively impact the growth of the global climate tech market. Global agreements, like the Paris Agreement, aim to reduce carbon emissions and are likely to drive high demand for climate tech solutions.

Moreover, companies’ efforts under corporate sustainability goals are further expected to accentuate the growth of the industry. Many organizations are working on net zero emissions which is likely to boost the growth of climate tech solutions in the market. Advancements in hydro, wind, and solar technologies are also anticipated to revolutionize the market in the coming years. Breakthrough improvements in energy storage technology are another major factor likely to support the growth trajectory of the industry. Rising investments from private equity firms and venture capital are encouraging the growth of climate tech start-ups which is also likely to support the growth of the industry.

However, the collaborative initiatives among different countries are likely to foster best practices in climate tech. For instance, GE Hitachi Nuclear Energy and TerraPower said to make a VTR program for the US Department of Energy in 2020. Engineers and scientists partnered in this program with their expertise in sodium reactor technology.

Restraints

- High initial investments are likely to hamper the growth of the global market.

Climate tech solutions involve high initial capital investment for energy systems and renewable energy infrastructure, which is a big barrier to the growth of the global market. Moreover, technological challenges are further expected to affect the growth of the industry. Technologies like carbon capture witness reliability and efficiency issues.

Opportunities

- Technology integration is likely to foster growth opportunities in the global market.

Integration of Internet of Things technology and artificial intelligence with climate tech solutions is likely to foster growth opportunities in the global climate tech market. These advancements are likely to improve data collection, analysis, and management activities which in turn is further expected to enhance the efficiency and effectiveness of the system. Emergence of blockchain technology offers more security and transparency in tracking carbon emissions and credits which in turn is also likely to positively impact the growth of the industry in the coming years.

For instance, Climeworks AG to unveil the start of its second large-scale direct capture plant in 2022. It is said to be built in the coming 18-24 months. It is expected to have the capability to suck 36,000 tons of carbon dioxide per year.

Challenges

- Supply chain and resource constraint is a big challenge in the global market.

Supply and production of certain materials like lithium witness price volatility and supply disruptions which is a major challenge in the climate tech industry. Moreover, the economic downturns in both the government and private sectors are further expected to slow down the growth of the industry.

Segmentation Analysis

The global climate tech market can be segmented into components, technologies, applications, and others.

On the basis of components, the market can be segmented into services and climate tech solutions. The climate tech solutions segment accounts for the largest share of the climate tech industry. Regulatory policies are the primary factor for the high growth rate of climate tech solutions. Growing number of companies are working on sustainability goals which is likely to drive the demand for climate tech solutions. Continuously growing technological innovations are making these solutions more cost-effective and efficient. Rising interest of investors in funding climate tech projects is also expected to foster growth opportunities in the segment.

Additionally, increasing awareness among people regarding sustainable products and services is also expected to positively influence the market dynamics. Moreover, advancements in solar, hydro, and bioenergy technologies are also anticipated to positively impact the growth trajectory of the segment.

On the basis of technologies, the market can be segmented into blockchain, security, cloud computing, digital twins, AI & analytics, IoT, and others. Blockchain is the fastest-growing segment in the global climate tech market. Blockchain is more transparent and offers secure transactions. Decentralized nature is highly needed in industries like supply chain, finance, and healthcare. Blockchain is highly adopted in financial services like instant payments, cryptocurrency, and small contracts and therefore, it is largely used by big organizaowing interest of startups is further anticipated to fuel the development of new blockchain applications. Automating smart contracts eliminates the requirement of any intermediaries, thereby saving costs and time for businesses.

On the basis of applications, the mations. Blockchain integration with emerging technology is further expanding its application in climate tech solutions. Rising adoption of blockchain by big organizations is also likely to bring more investments in the segment. Grrket can be segmented into sustainable mining & exploration, weather monitoring & forecasting, forest monitoring, crop monitoring, water purification, carbon footprint management, and green building. Carbon footprint management segment is likely to swipe the largest share in the climate tech industry during the forecast period. Strict regulations are the primary growth factor in the segment. Government mandates to lower greenhouse gas emissions are forcing organizations to adopt carbon footprint management solutions.

Moreover, companies are establishing sustainability goals like zero-emission or carbon neutrality under corporate sustainability goals, which in turn is also likely to positively impact the growth trajectory of the segment. Additionally, the rising demands from stakeholders and investors for sustainable and transparent business practices are further likely to create demand for carbon footprint management solutions.

The consumer awareness regarding the environmental impact of production operations is further expected to positively impact the growth of the segment. Technological advancements like AI, IoT, and data analytics are further improving the accuracy of these solutions which in turn is widening the scope of the segment in the coming years.

However, these carbon management solutions help in long-term cost saving while lowering waste and improving the energy efficiency. Moreover, increasing collaboration between technology providers, corporations, and the government is further expected to encourage the adoption of power management solutions in the market.

Report Scope

Report Attribute |

Details |

Market Size in 2023 |

USD 20.06 Billion |

Projected Market Size in 2032 |

USD 47.29 Billion |

CAGR Growth Rate |

10.00% CAGR |

Base Year |

2023 |

Forecast Years |

2024-2032 |

Key Market Players |

Hortau, Cropx, Consensys, Trace Genomics, Taranis, Isometrix, Lo3 Energy, Sensus, Enviance, Intelex, Engie Impact, Schneider Electric, Microsoft, Salesforce, Enablon, IBM, GE, and Others. |

Key Segment |

By Components, By Technologies, By Applications, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Regional Analysis

- North America to dominate the global market.

North America will account for the largest share of the global climate tech market during the forecast period. Federal and state policies like the Inflation Reduction Act are encouraging the adoption of carbon reduction techniques, which in turn is a major reason for the high growth rate of the regional market.

However, Canada’s climate action plan is another major step towards the goal of lowering greenhouse emissions with the help of investments in green technologies and subsidies for adopting renewable energy. North American companies are looking forward to aligning with net zero emissions under corporate sustainability initiatives.

Such initiatives are likely to draw more investments in climate tech solutions for carbon management and energy efficiency. The region is a hub for technological innovation in energy storage, electrical vehicles, renewable energy, and carbon capture technologies. Also, the advancements in blockchain, IoT, and AI are further expected to push the deployment rate of climate tech solutions in the region.

Asia Pacific is also dominating the climate tech industry because of government policies, technological advancements, and investments in sustainable technology. China is leading the regional market with a significant amount of investments in energy storage. Electric vehicles and energy initiatives by the government are supporting the regional market on a large scale to help companies achieve power neutrality goals.

However, India is also likely to contribute significantly towards the growth of the regional market because of the expanding renewable energy capacity in wind and solar power. Japan and South Korea are the hub of technological innovation thereby leading the market in energy efficiency, smart grids, and hydrogen economy, which in turn is also expected to revolutionize the market in APAC.

Additionally, South Asian markets like Thailand, Vietnam, and Indonesia are also making efforts to invest in renewable energy and sustainable infrastructure. All these factors are likely to promote climate tech solutions in the Asia Pacific market.

Competitive Analysis

The key players in the global climate tech market include:

- Hortau

- Cropx

- Consensys

- Trace Genomics

- Taranis

- Isometrix

- Lo3 Energy

- Sensus

- Enviance

- Intelex

- Engie Impact

- Schneider Electric

- Microsoft

- Salesforce

- Enablon

- IBM

- GE

For instance, Mohamed bin Zayed University of Artificial Intelligence decided to build an AI center of Excellence in partnership with IBM in 2023. This center was successfully established during the World Future Energy Summit that was held in Abu Dhabi Sustainability Week.

The global climate tech market is segmented as follows:

By Components Segment Analysis

- Services

- Climate Tech Solutions

By Technologies Segment Analysis

- Blockchain

- Security

- Cloud Computing

- Digital Twins

- AI & Analytics

- IoT

- Others

By Applications Segment Analysis

- Sustainable Mining & Exploration

- Weather Monitoring And Forecasting

- Forest Monitoring

- Crop Monitoring

- Water Purification

- Carbon Footprint Management

- Green Building

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

- Hortau

- Cropx

- Consensys

- Trace Genomics

- Taranis

- Isometrix

- Lo3 Energy

- Sensus

- Enviance

- Intelex

- Engie Impact

- Schneider Electric

- Microsoft

- Salesforce

- Enablon

- IBM

- GE

Copyright © 2023 - 2024, All Rights Reserved, Facts and Factors